Read our latest Investment Strategy summary for the first quarter of 2024, which reflects on all the key Macro indicators and Geopolitical influences on Global Stock Markets, Fixed Income, and Commodities.

Global Stock Markets

In 2023 there were two distinct periods of rising volatility: During the March Banking Crisis and in October on the horrific escalation of the Gaza-Israel conflict. The recession calls many investment houses gave at the start of the year, have not materialized, as the US had a particularly strong third quarter.

However, economic activity has considerably slowed in Q4, what was likely behind the FED’s motivation to pivot. Europe’s and Japan’s economies have remained lacklustre at best, while China has been facing deflation.

The key development in 2023 was the euphoria around Artificial Intelligence, what created a bullish atmosphere in technology stocks, even as interest rates had continued to rise.

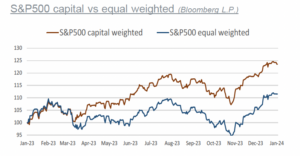

The Magnificent Seven, AAPL, AMZN, GOOGL, META, MSFT, NVDA, TSLA, accounted, at times, for three quarters of the S&P500 performance. This disproportionate weight of the large-cap tech stocks requires special attention, as the potential for outsized gains and risks are both amplified by this concentration.

Given the renewed recession risks, the analysts expectation of 10% earnings growth in 2024 seem challenging.

The MSCI USA Index has approached its record, but it remains to be seen whether it can be surpassed on a sustained basis.

The MSCI China Index has seen a persistent decline, following the recovery high in late last January, despite various efforts to boost growth. European equities experienced a strong rebound in Q4 too, ending the year on a high note. Whereas the Swiss and UK indices were basically sideways for the year.

So diverse were the various trends! The dominance of large tech stocks and the rise of passive investing have created a symbiotic relationship, with the tech giants benefitting from a steady influx of capital from index funds.

In the week of the December FED meeting the world’s oldest and largest ETF, State Street’s SPDR S&P500 ETF, saw the biggest inflow since inception, more than $24bn.

Another record was set in the same week, when $5 trillion in US stock options expired, 80% in S&P500-linked contracts. Options trading volume have continued to increase significantly.

The option markets have become the tail wagging the dog. Volume has been boosted in part by the popularity of ETFs that sell options to generate income.

The use of options and the rise of passive investing, whose share of US stock markets is now estimated to be 45%, has led to a sea change in investment framework.

2023 has turned out to be by far not as bad as feared. The current macro backdrop has been a typical late cycle environment. It has been a slow moving cycle vs fast moving media.

With the wisdom of hindsight, the essential points to grasp were, that the US was not yet going into recession, that China would not rebound from its Covid restrictions particularly fast and that the conflict between Russia and Ukraine would not have a significant impact on energy prices.

A year ago headlines were full of Sam Bankman-Fried and FTX. The implosion was only the most spectacular in a series of scandals.

In hindsight, the extreme negativity of sentiment proved to be a great entry point in Bitcoin.

The eyes from the crypto space are on January 10, when US regulators must decide whether to give the OK to a physically-backed Bitcoin ETF.

Global Fixed Income Markets

Two years ago investors were convinced the tightening cycle would be gradual and controlled.

However, the burgeoning inflation and subsequent 525bps of rate hikes had proved otherwise.

After hiking in July by 25bps, the FED delivered a so-called hawkish pause at the September meeting, leaving the target range at 5.25% to 5.50%. Yet, it signalled that another hike for 2023 might be in order.

At the November meeting the FED shifted its tone, that it was in no hurry to raise rates further. Weak October jobs report delivered the confirming signal, unleashing a rally in bonds and equities. At the December meeting the FED at last executed the much discussed policy pivot.

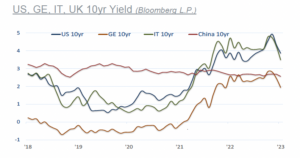

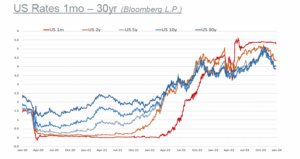

Bond yields made a roundtrip in 2023, as November was the best month since 1985. Bloomberg Global Aggregate Treasury yield fell from the cycle high at 3.65% in October to below 3%, where it was at the beginning of the year.

The US 10yr yield, after hitting 5%, closed the year at 3.78%, while the US 2yr yield finished at 4.24%. The yield curve became less inverted.

At its extreme, the 10yr yield was 110bps lower than the 2yr. This dichotomy between short-term monetary policy and long-term growth and inflation expectations had been persisting since 2022.

We see a bull steepening scenario, where the short-term rates fall faster than the long-end; steepening the yield curve.

The FED’s beige book, a summary of commentary on current economic conditions by the twelve FED districts, was released at the end of November. It was the precursor to the FED moving away from its “higher for longer” stance.

The report read, that on balance, economic activity slowed since the previous report, with four districts reporting modest growth, two indicating conditions were flat to slightly down, and six noting slight declines in activity.

With inflation down across the world, the peak is in for most central banks, and talks have turned to cuts. In the US, inflation was 9% a year ago; it’s now around 3%. In Europe, it has fallen from 10% to less than 3%. The dot-plot’s of rate projections by the FED officials showed a median estimate of 75pbs cuts in 2024.

The market is even pricing in a total of 150bps cuts. The FED is likely to make good on market pricing for a cut in March. The ECB could be on a similar timetable and cut in March too. The market even sees a greater potential than 150bps cuts in Europe. The Bank of England faces a different situation by the fast wage growth.

Yet, the market is pricing in a cut by June and about 150bps by the end of the year. The Bank of Japan on the other side, is seen sticking to the yield curve anchor through the first half. At the end, the question will be, can the FED just lower the rates, or will the FED have to lower the rates. The bond market sees growth falling faster, than the FED anticipates.

US Dollar

The Dollar remains the name of the game. During the March banking crisis and the eruption of the Gaza conflict it had been strengthening.

With the risk on rally since the beginning of November, it had weakened. However, with the turn of the year there is already a lot of tensions building in the FX markets again.

The emerging markets currencies could not really profit from the Dollar’s weakness, closing the year near the lows. What is indicative of Dollar problems in these parts of the world. The Dollar’s share of payments via SWIFT increased to 47% from 42% last year. Euro’s dropped from 36% to 23%, Yuan increased to 4.6% from 2.1%.

Commodities, Macro

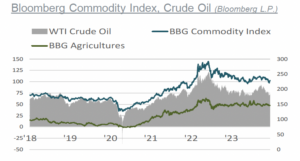

The Bloomberg Commodity Index ended the year down -13%. The energy sub-index was the weakest, -25%, while the precious metals’ was up 4%. The industrial metals sub-index kept the lacklustre posture, copper ended the year basically flat.

Agricultures were mixed. Corn and wheat were down by -30%, respectively -22%, while Cocoa was up 65%, finishing at the highest annual close. Gold soared to an all-time high in early December, setting a new mark at 2135.

Gold as primarily a store of value and safe-haven for many has the fourth push against the $2000 level. It will be interesting to see how things evolve in the first quarter. However, Silver so far has failed to confirm a bullish trend.

Speculation has certainly played a role, in both, driving WTI crude oil up to $95 in late September and then down to $68 by mid-December. Speculative positions were at a two-year high in September, then dropping to the lowest in recent years.

A series of negotiated cuts by OPEC+, including the latest voluntary cut of 2.2mbd, which came amid delayed meetings and lots of drama failed to halt a slump in prices. Despite good demand growth, US supply growth and broad non-OPEC had been stronger than anticipated.

However, the recent flare-up of tensions in the Middle East could reintroduce a conflict premium for oil.

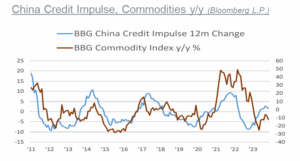

The commodity cycle isn’t likely over, despite investor’s concerns about weak demand in the short-term due to recession risks. The supply side issues and the lack of investments in recent years have not all been resolved.

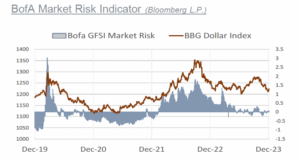

Geopolitical deterioration has significantly increased tail risks for economies and financial markets.

The world hasn’t witnessed such a rapid change in the geopolitical landscape since 1989. A major war with Russia, the conflict in the Middle-East, the emergence of BRICS as a major political and economic bloc, energy security and increased political and ideological divisions in the West. We keep the recommended tactical allocation in commodities at neutral.

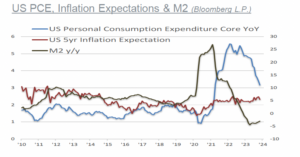

Market-based inflation expectations have stayed closer to 2% for most part since the beginning of 2021. The expected disinflationary forces have been playing out in full force.

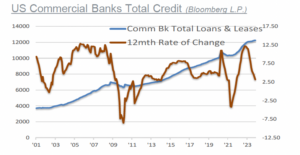

US headline inflation data and the FED’s favorite measure PCE have slowed significantly from their 2022 peaks. Leading indicators have been showing recession for some time. Credit data, such as NPL, credit surveys and financial ratios continue to be weak. Consumer credit has been particularly weak.

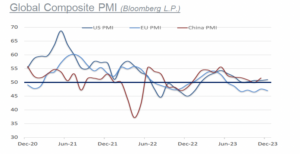

Global PMI survey data by S&P Global continue to show, that manufacturing still struggles. US December Manufacturing PMI fell to 47.9 from 49.4 in November, on lower output and falling orders. Eurozone’s Manufacturing PMI remained in deeply contractionary territory at 44.4 from 44.2 in November. It’s the 18th consecutive month of contraction.

After Fitch had downgraded the credit rating of US government debt in August, Moody’s lowered the outlook from stable to negative in December. Moody’s cited the political polarization in Congress and general concerns about the rising national debt. While that decision will have no consequences for the Dollar’s global role, it highlights the darkening fiscal outlook and the governance challenges.

The absence of any political will to deal with the drivers of the deficit. That is not just an US problem. The debate about fiscal dominance, where budget deficits overpower central banks effort to reign inflation, will intensify. Moody’s also downgraded the outlook on China’s credit rating from stable to negative due to concerns about the country’s post-pandemic recovery, weak consumer and business confidence, a persistent housing crisis, and a global economic slowdown.

The government debt to GDP for the advanced G20 nations rose from 80% to above 130% in 2020. The Covid-19 pandemic response resulted in a 20% increase alone. Japan has the highest government debt-to-GDP ratio at 255%, followed by Greece at 168% and Singapore at 168%. Italy’s government debt to GDP ratio is 144%, while the United States is at 97%. Saudi Arabia has the lowest government debt-to-GDP ratio among the advanced G20 nations, at around 41%.

Overall, the high levels of government debt in some advanced G20 nations raise concerns about their longterm sustainability and potential impact on economic growth.

Inflation, Tactical Allocation

While inflationary forces are structural and secular, on higher debt-load, demographics, on-shoring and friendshoring of manufacturing, the cyclical forces of deflationary potential will remain predominant in the first half. The dynamics of economic growth and inflation since the pandemic are different.

The world experienced an unprecedented flood of fiscal and monetary stimulus. Central banks were initially slow to respond. Real rates have only moved into positive recently. The dampening effects from positive real rates on growth and finances have yet to be fully seen.

That the narrative has been about soft landing for some time now, is in itself a sign that something is not quite right. That a recession didn’t happen by now, doesn’t mean it won’t happen.

For the past fours years the market has transitioned away from the 40-year trend of falling interest rates. Central banks have embarked on the most aggressive interest rate hike cycle since the early 1980s. Global disinflation momentum looks intact.

In our Q4 report we correctly anticipated that central banks were at the end of this hiking cycle. The question will be, can the FED just lower the rates or will it be compelled to do so in response to weaker economic conditions.

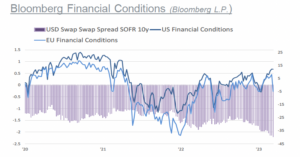

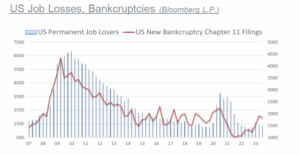

One fifth of global corporate bonds in issue are to mature by 2025. Global financial conditions have shifted rapidly. Debt restructuring are likely to become more frequent. So far, credit markets have remained relatively unworried about the financial stress and the recession risks. However, as bankruptcies have risen and credit availability is quite low, the pressure for credit spreads to widen will increase.

We keep our overweight allocation in fixed income. We start the year neutral on high yields and keep our preference for investment grade. The disinflationary period has not run its course yet. The historical pattern favors the bond market.

In the period following the end of a tightening cycle, investment grade bonds delivered a positive performance relative to equities. All that, while equity benchmarks trade at elevated valuations.

What is clear, central banks face the challenge of recession risks within a time of secular inflation. They need to strike the balance between financial stabiliy vs. price stability. The next few years will be characterized by the central banks constantly braking, relasing the brakes and accelerating.

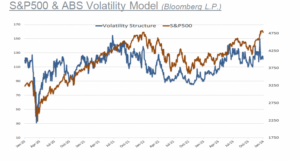

S&P500 & Volatility

A soft landing is the desirable outcome. However, the markets configuration implies, that the potential for monetary deflation is high. We start the year neutral on equities.

We are overweight on US, neutral on Europe, underweight on China and Emerging Markets. After 2022’s deleveraging phase, 2023 brought the disinflation rebound. While at the start of the year GDP forecasts were close to zero, things turned out to be more positive.

Following three quarters of negative earnings growth, earnings per share increased by more than 5% in Q3, on the resurgence in the big tech stocks earnings.

However, the expectations for 10% earnings growth in 2024 seem challenging, given the current macro-economic backdrop. The full effects of the hiking cycle on growth have yet to be seen.

It’s vital to understand that a mixed environment can be confusing at times. We focus on high quality, while diversification is key. At any rate, there will be opportunities ahead.