Global Stock Markets

In the third quarter, investors’ eyes were firmly on central banks, while the dire geopolitical developments had no significant impact on financial markets. At the beginning of August, the Japanese stock index Nikkei lost 12.4 percent, the largest daily loss since 1987, after the Bank of Japan raised the key interest rate again.

The BOJ had previously raised the rate in March for the first time in eight years from -0.1 to 0.1%. The unexpectedly strong rise in the Yen and weak US jobs data in July triggered a wave of selling in US and European stocks. The so-called Yen carry trade, which had ballooned over the years, where money is borrowed in Yen and invested in higher-yielding assets, such as US Treasuries and stocks, had to be unwound almost abruptly. The turbulence did not last long.

In mid-August, good US retail sales meant that US recession concerns faded into the background. The Yen also stopped its upward trend. At the annual central banks meeting in Jackson Hole at the end of August, FED Chair Jerome Powell announced ‘that the time has come for policy to adjust’.

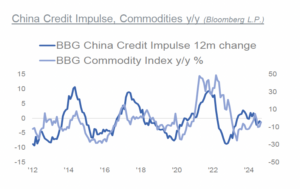

Stock markets had to overcome a weak start to September, before then the FED followed with a jumbo cut of half a percentage point, setting the new range at 4.75 – 5.00%. In the final week of September, the People’s Bank of China announced a blitz of easing measures to restore confidence. The Politburo stated unequivocally that efforts should be made to stabilise the real estate market and stop the decline and the associated negative impact on consumption and the economy.

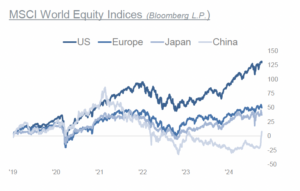

The announcements sparked a massive rebound in Chinese stocks. The economic slowdown in China is weighing on the world, which is causing concern among European companies in particular. What will be crucial, however, is that the Chinese government will deliver fiscal measures in addition to the monetary stimulus.

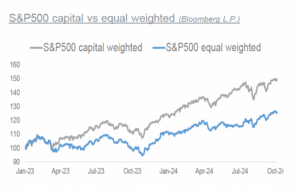

The stock markets have performed much better so far than most expected at the start of the year. The S&P500 closed the third quarter at a new all-time high, up 21% since the start of the year.

However, it is still led by the semiconductor sector, although the tech-heavy Nasdaq is still below its July high. The expectation of monetary easing led to a rotation into other sectors, such as defensive and value stocks. This improved the market breadth and reduced the dependence on the big tech stocks. Which is a positive. Three risks still have to be considered.

The geopolitical situation has worsened again in the Middle East and in Ukraine. The US political situation has become more unpredictable, as it is a very close contest. Harris’ economic plans are geared towards the middle class, she wants to raise corporate taxes.

Trump favours higher tariffs, less regulation and lower taxes. Both will lead to higher budget deficits and higher debt. European assets are facing headwinds from political uncertainty and exposure to the struggling Chinese economy.

Global Fixed Income Markets

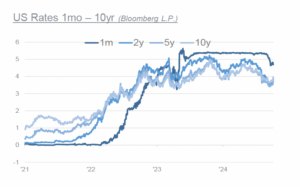

We noted in our Q3 letter, that June was the first month in four years, that no central bank hiked rates. And indeed, this marked the transition to a consistently positive third quarter for the bond markets.

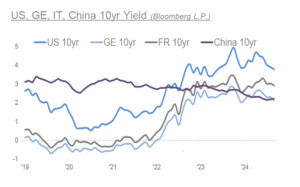

The shift in investors’ expectations for interest rates helped bonds to perform strongly. The US 10yr yield fell from 4.39% to 3.78% over the quarter, while the 2yr yield fell from 4.75% to 3.64%.

In early September the 2yr yield fell below the 10yr for the first time since July 2022. This ended the longest period ever, that the yield curve had been continuously inverted, that short-term bonds yield more than longer ones. That exceeds a record 624 day inversion in 1978. Unlike in 2022, the negative correlation between stocks and bonds was evident in early August, when a sharp correction in global risk assets was partially offset by an increase in government bond prices.

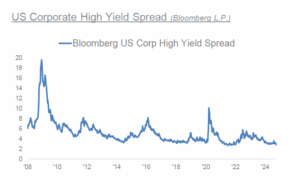

Safe-haven assets like US Treasuries saw increased demand. Credit markets also performed strongly. High yield spreads have narrowed back to levels seen at the end of 2021. Investment grade spreads have even narrowed to the tightest levels in 20 years.

In the US, the combination of a stronger-than anticipated decline in July’s non-farm payrolls, the unemployment rate trending higher, and a larger than expected drop in inflation in August, caused the FED‘s decision to begin its long-awaited cutting cycle with a 50 bps move to 5.00-4.75%. The FED cited, that risks to employment and inflation have become balanced, that upside risks to inflation have diminished and downside risks to employment had increased.

The FED stated, that it is committed to support maximum employment. The FED’s median rate projections for 2024 were at 4.4%, while for 2025 it was at 3.4%. We expect the FED to make good on the projection and will deliver two more 25 bps cuts at the last two meetings this year.

The ECB has so far cut interest rates in two steps by 25 bps each, in June and September. In contrast to the FED, the need for action at the ECB is increasing. Eurozone inflation fell to 1.8% in September, below the threshold of two percent. Although core inflation is still at 2.8%, the ECB is challenged, given the increasingly weak economic data.

Germany recently revised its economic forecast for 2024 downwards, to -0.2% from 0.3%. These two major central banks have changed course and are lowering interest rates. And yet, questions remain: How will the Bank of Japan proceed to normalise monetary policy; it ended eight years of negative interest rates last March. What will be the effects, if China decides on fiscal measures in addition to monetary stimulus?

US Dollar

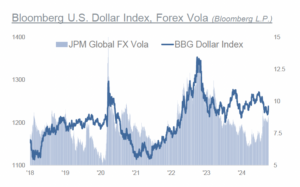

The Dollar remains the name of the game. That may sound trite, but it remains central to the capital markets. With the prospect of rate cuts in the US, the Dollar softened. That has helped. However, volatility in FX markets, as measured by the J.P. Morgan Global FX Volatility Index, has continued to trend higher since spring.

Eyes are not just on the Japanese Yen and the Chinese Yuan. The Indian Rupee has fallen to a new all-time low vs. the Dollar. According to Bloomberg, the Dollar’s share of payments via SWIFT increased to 49.7% from 41.8% since 2023. Euro’s dropped to 21.6% from 36.3%, Yuan increased to 4.7% from 2.1%.

Commodities

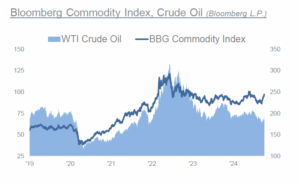

The Bloomberg Commodity Index was slightly down on the quarter. Energy was the weakest component of the index due to lower global demand, falling by -13%, despite the geopolitical problems. Industrials and agricultures are slightly up. Precious metals are up 10%. Gold has continued to new all-time highs, moving above $2’600. While Silver remains up 30% since the start of the year.

Index was slightly down on the quarter. Energy was the weakest component of the index due to lower global demand, falling by -13%, despite the geopolitical problems. Industrials and agricultures are slightly up. Precious metals are up 10%. Gold has continued to new all-time highs, moving above $2’600. While Silver remains up 30% since the start of the year.

We wrote in our Q4 2023 report that Gold, as primarily a store of value and safe-haven for many, could well see an interesting 2024, as it was pushing against the $2’000 level for the fourth time last December. Central banks have been notable buyers of Gold, which has surpassed the Euro to be the top reserve currency, behind the Dollar.

While the data from the largest Gold-ETFs continue to show that investors have a significantly lower exposure to Gold than during the previous three times Gold had moved to new highs. All four sub-indices have been higher since the beginning of September.

Global and US oil demand growth next year is expected not to meet prior forecasts due to weakening economic activity in China and North America. While the big three agencies, OPEC, IEA and EIA, differ in their demand growth forecasts, the U.S. Energy Information Administration expects the US, currently top oil producer in the world, to pump less. A topic we discussed here before, whether US production growth will be sustainable.

AI’s growing demand for power, will add to the investment case for key metals. Whether copper for grid expansions and upgrades, or uranium to meet growing low-carbon energy needs.

We keep the recommended tactical allocation in commodities at neutral. We remain strategically positive on precious metals. However, we would not be surprised, should Gold enter a temporary consolidation phase. We upgrade agricultures to overweight. The move higher since summer has a bullish appearance.

Macro

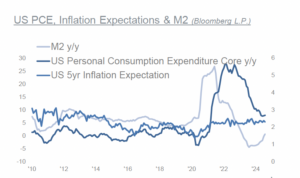

Market-based inflation expectations have stayed closer to 2% for the most part since the beginning of 2021. The expected disinflationary forces have been playing out. US inflation data have slowed significantly from their 2022 peaks. US headline inflation data has fallen to 2.4% y/y. However, PCE has not made any progress to downside in recent months, it remained at 2.7% y/y since May.

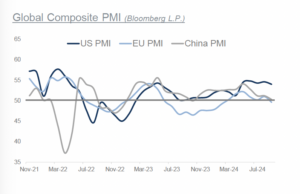

Latest PMI data signal the slowest global expansion since January. Optimism hits near two-year low. The headline JPMorgan Global PMI, covering manufacturing and services in +40 economies, fell from 52.8 in August to 52.0 in September, to its lowest since January. It stood at 53.7 in May.

The soft landing scenario prevails, as the macroeconomic outlooks seems clearer. It remains our base case. However, we are aware that when there’s too much consensus around a particular outcome, it can sometimes be a warning sign, that people are overlooking potential risks or alternative scenarios. The risks of an economic slowdown haven’t entirely gone away.

The surveys of new orders from the various Fed districts still show on aggregate a negative reading. It’s important to remain adaptable to changing economic conditions.

The Treasury Department, to finance the fiscal deficit of 7%, had offset the FED’s quantitative tightening by increasing the share of total issuance for Treasury Bills beyond the norm.

During the second quarter that had normalised. However, In July and August there was a sizeable uptick in issuance of T-Bills relative to bonds.

Overall, recent data suggests global liquidity has continued to increase. However, over the turn of the quarter funding and market liquidity seemed to have turned lower. Sensitive repo rates jumped relative to FED funds, what was potentially signalling shortages of collateral.

It is important to have an eye on the MOVE index, a measure of US bond market volatility. It has surpassed the level of 100; above the traditional norms of around 70. A higher MOVE influences the efficacy of the collateral pool.

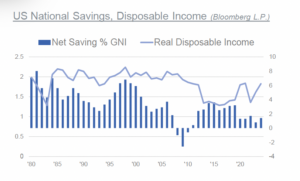

The government debt to GDP for the US stands at 122%, in Japan it is 260%. These high

levels of government debt raise concerns about their long-term sustainability and potential impact on economic growth. It highlights the darkening fiscal outlook and the governance challenges.

There is no political will to deal with the drivers of the deficit, as that would come with economic costs. For the developed markets it is rather unique, they are less used to an environment of fiscal dominance.

The impact from increased government’s share show, that over the last two decades, real GDP per capita has been declining. Today, the net national saving has gotten close to negative.

Tactical Allocation

The inflationary forces are structural and secular, on higher debt-load, demographics and on-shoring of manufacturing. We are currently in an interim period. In our Q4 2023 report, we correctly anticipated that central banks were at the end of the hiking cycle. Yet, the FED was not forced to act, as the economy proved resilient.

The picture has changed. The market expects the FED to cut further at its last two meetings this year. We keep our overweight allocation in fixed income.

We stay neutral on high yields and keep our preference for investment grade. Selectivity and diversification is key. We are mindful of the developments in the commodities.

S&P500 & Volatility

A soft landing is the desirable outcome. But sometimes one should be careful when an overwhelming majority expects the same. However, as things stand, we don’t see the macroeconomic situation to be changed a lot in the fourth quarter. Expectations for the upcoming US Q3 earnings season call for 4-5% earnings growth.

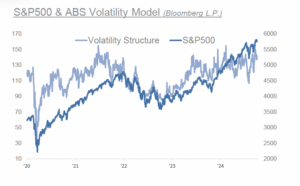

This compares to 11.6% growth in Q2. Analysts expect earnings of the big techs to grow 20%, but a contraction of -20% for energy. These are some key figures that need to be monitored. Volatility measures have started to diverge from the trend in stocks, as they often do after the end of a quarter. What could be an early indication that the markets could experience a technical pull back.

This time, however, the US elections are around the corner! We favour a neutral allocation in equities. We cut US to neutral, remain neutral on Europe and China, and underweight on Japan. While there is no historical analogy to the current environment, we focus on high quality and diversification remains key.

Allocation Recommendations