Global Stock Markets

The US stock market has kept its strong posture from the fourth quarter. European and Japanese markets followed suit. The Chinese stocks only started to rebound in February after officials intensified efforts to stem the market rout. What could potentially have ended a three-year bear market in China.

US equities closed the first quarter strong. The S&P500 gained 10%, surpassing the 5200 level for the first time in March. Improving fundamentals propelled the strong performance.

Better headline data from the jobs report, S&P500 companies beating earnings estimates by a healthy 4% and the continued relief on inflation, are seen as the primary factors. Equally important has been the continued loose fiscal policy, which has balanced out the FED’s tightening policy. Optimism about a soft landing scenario has prevailed.

Expectations of interest rate cuts have helped sentiment, although the pace of cuts is likely slower, than what markets were pricing in at the start of the year. Technology stocks continued to drive the market, amid ongoing enthusiasm around Artificial Intelligence.

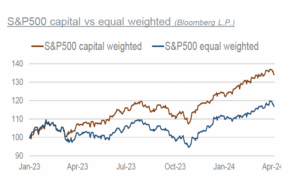

However, only four of the ‘Magnificent Seven’ continued to lead the market, with Nvidia’s performance standing out. It is worth noting, that the market breadth did improve some, as compared to last year’s very concentrated leadership. In 2023, the widespread worries that the FED’s rapid interest rate hikes might trigger a recession proved wrong. The banking crisis a year ago did not become the tipping point. On the other hand, do equity prices in 2024 reflect near perfection? That cannot be affirmed.

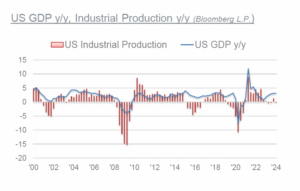

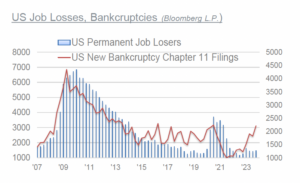

The US economy has avoided recessionary signs in Q1. Most economic forecasts show optimism. It’s a tale of two economies, as most top tier-data as GDP and jobs show a resilient economy, corporate default rates and consumer delinquencies paint a different picture.

The proliferation of passive investment strategies has led to some distortion in the forward-looking information in equity and credit markets. The significantly increased options trading volume has further impacted how market dynamics and risk assessments have evolved.

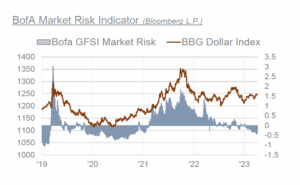

The hugely increased use of options, and the rise of passive investing have led to a sea change in investment framework. Global passive equity funds’ net assets surpassed those of their active counterparts for the first time in 2023. At any rate, measures of financial conditions improved in line with rising equities.

The long awaited approval by US regulators to give the OK to physically-backed Bitcoin ETF was given in January. The days following the SEC’s announcement Bitcoin saw a knee-jerk reaction to the downside, dropping below $40’000. By mid-March Bitcoin traded above $70’000. Inflows into these ETFs have been substantial since. Bitcoin has seen strong demand and growing institutional interest. The escalating geopolitical situation did not have much of an impact on financial markets.

Global Fixed Income Markets

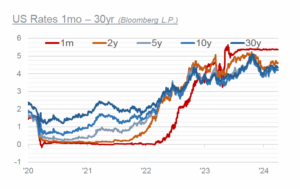

Unlike the stock markets, bonds gave back some of their strong gains incurred in the last quarter of 2023, after the peak was in for most central bank rates. Following a string of ‘hotter’ US inflation data, the bond market aligned with the FED’s view of three cuts, 25bp, for 2024.

At the start of the year, the market had a total of 150bp of easing priced in. It had expressed near certainty, that the FED would start cutting rates as early as in March. At the March meeting the FED confirmed its easing bias, reiterating three cuts.

March made for an interesting month for monetary policy. The ECB confirmed its June rate cut signal. The Bank of England indicated, it is headed for a mid-Year pivot as well. Turkey shocked with a jumbo hike of 500bp to 50%. Many see this as a pivot toward credibility, away from political control.

The Swiss National Bank surprised by becoming the first of the developed countries to cut rates, setting the policy rate to 1.5% from 1.75%, as year-over-year inflation has fallen to 1%.

The Bank of Japan ended its Negative Interest Rate Policy, that lasted for eight years. It raised the benchmark rate from -0.1% to 0.1%, what

marks the first hike in 17 years. It further abandoned its Yield Curve Control and seized the purchases of ETFs and REITs. It will continue the purchases of government bonds, yet not specifying future steps of this long normalization.

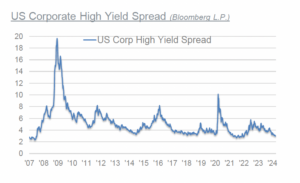

Credit markets are acting as if there were no interest rate hikes. Spreads between junk bond yields and investmentgrade counterparts are tight. In some cases, the tightest since GFC. The compensation for yield on bonds with ‘high’ risk compared to ‘moderate’ risk has been not of a concern. Not surprisingly, as high yield markets have high correlation to equities, which have moved to new highs.

However, it’s a segment that needs to be observed. For now, things are ok, as recession fears have receded, monetary easing hopes are alive and net issuance of new junk bonds have fallen short of demand. In terms of tight spreads, credit markets are in bubbly territory, currently only 200bp between junk and BBB. That compares to 700bp during the pandemic lockdown and more than 1300bp during the GFC.

The commercial real estate situation in the US still looks unmanageable. Any crack in the US economy or weakness in the labour markets should be monitored. It’s like with volatility; low volatility presedes periods of high volatility. Tight credit spreads precede periods of wider spreads. It’s just not possible to perfectly time the impending shift.

US Dollar

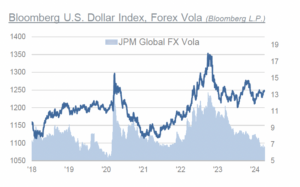

The Dollar remains the name of the game. That may sound trite, but it remains central to the capital markets. It had ended 2023 on a weak note. However, we wrote in the Q1 report, that with the turn of the year, tensions were building in the FX markets again. That observation proved correct. The Dollar is up vs major currencies.

According to Bloomberg, the Dollar’s share of payments via SWIFT increased to 47.5% from 41.8% in 2023. Euro’s dropped to 23.4% from 36.3%, Yuan increased to 4.1% from 2.1%

Commodities

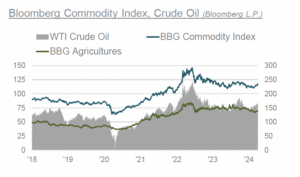

US shale oil production has grown significantly over the last +10 years. US shales met more than 100% of global demand growth. It has been the key source of non- OPEC growth. However, question marks arose on how sustainable US production growth will be.

While oil markets have been broadly balanced over the last year, upcoming reports on US production will need to be looked at closely. As it seems, the risks are pointing to a slowdown of production growth. The odds of $100 oil are rising again. The US Energy Information Administration, after forecasting global inventories to remain unchanged, now see’s them fall by 900’000 barrels a day.

Brent Oil jumped above $90 on military tensions between Israel and Iran. However, fears of a global supply shock are returning, that could s

park a resurgence of commodity-driven inflation. OPEC+ announced that they will be extending their voluntary oil output cuts of 2.2 million barrels per day into the second quarter of 2024.

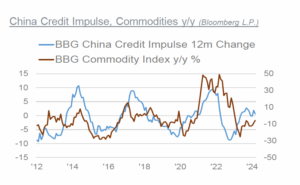

The group has decided to keep production cuts unchanged until the end of the first half of the year. The Bloomberg Commodity Index trades at the highest since last November, with all subsectors recovering from the mid-February cycle lows. In industrial metals, copper, lead and nickel are higher.

Within agriculture, Cocoa continued the massive run up, reaching $10’000 per metric ton. It has surged 120% since the start of the year on supply shortage in West Africa. Gold has moved to new all-time highs as well, moving above $2’300.

We wrote in our previous report, that Gold, as primarily a store of value and safe-haven for many, could well see an interesting first quarter, as it was pushing against the $2’000 level for the fourth time. In 2023 central banks have been notable buyers of Gold.

While the data from the largest Gold-ETFs show, that investors have a significantly lower exposure to Gold than during the previous three times Gold pushed against $2’000. We keep the recommended tactical allocation in commodities at neutral, but we are overweight to precious metals.

Macro

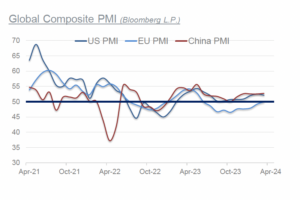

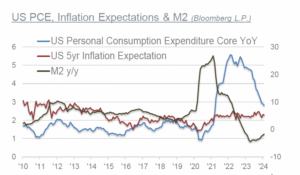

Market-based inflation expectations have stayed closer to 2% for most part since the beginning of 2021. The expected disinflationary forces have been playing out. This trend should continue in Q2. But perhaps it is time to consider that this is not a situation that lasts forever. US headline inflation data and the FED’s favorite measure PCE have slowed significantly from their 2022 peaks. Some leading indicators have been showing signs of improvement, after having been in recession for some time. Global PMI survey data by S&P Global showed a further modest acceleration of global economic growth.

Market-based inflation expectations have stayed closer to 2% for most part since the beginning of 2021. The expected disinflationary forces have been playing out. This trend should continue in Q2. But perhaps it is time to consider that this is not a situation that lasts forever. US headline inflation data and the FED’s favorite measure PCE have slowed significantly from their 2022 peaks. Some leading indicators have been showing signs of improvement, after having been in recession for some time. Global PMI survey data by S&P Global showed a further modest acceleration of global economic growth.

The soft landing scenario prevails, while economic uncertainty remains high. The risks of an economic slowdown later in 2024 haven’t gone away. In fact, the surveys of new orders from the various Fed districts showed a decline in March. We wrote before, that fiscal policy took over from monetary policy. That the debate about fiscal dominance, where budget deficits will overpower central banks effort to reign inflation, will intensify at one point.

The FED has moved on to the tightening cycle, by letting maturing bonds slip off its balance sheet, instead of reinvesting into new issues as it had previously done. The Treasury Department, on the other hand, to finance the fiscal deficit of 7.5%, has offset the quantitative tightening by increasing the share of total issuance for Treasury Bills beyond the norm.

The FED has moved on to the tightening cycle, by letting maturing bonds slip off its balance sheet, instead of reinvesting into new issues as it had previously done. The Treasury Department, on the other hand, to finance the fiscal deficit of 7.5%, has offset the quantitative tightening by increasing the share of total issuance for Treasury Bills beyond the norm.

By changing the amount of interest-rate risks provided to the markets, it has actively intervened, and provided liquidity. As Treasury Bills are short-term assets with no credit risk and no duration risk. Banks and investors absorbing duration risk, have likely to reduce the risk they take elsewhere.

Historically, bills issuance have made up 20%, whereas so-called coupons issuance, maturities from 1-30 years, have been four times larger. This relationship has been reversed since last summer. The government debt to GDP for the US stands at 120%, for the Eurozone at 112%.

In Japan it’s above 200%. These high levels of government debt raise concerns about their long-term sustainability and potential impact on economic growth. It highlights the darkening fiscal outlook and the governance challenges. There is no political will to deal with the drivers of the deficit, as that would come with economic costs. For the developed markets it is rather unique, they are not used to an environment of fiscal dominance.

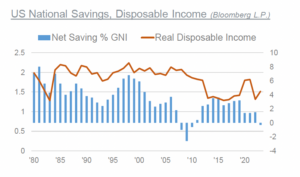

The impact from increased government’s share show, that over the last two decades, real GDP per capita has been declining. Today, the net national saving is negative. Something that happened only during GFC and the 1930s. The ramifications are reduced investments and declining living standards.

The impact from increased government’s share show, that over the last two decades, real GDP per capita has been declining. Today, the net national saving is negative. Something that happened only during GFC and the 1930s. The ramifications are reduced investments and declining living standards.

Tactical Allocation

While inflationary forces are structural and secular, on higher debt-load, demographics, on-shoring of manufacturing, the cyclical forces of deflationary potential have been less dominant than expected. In our Q4 report, we correctly anticipated that central banks were at the end of the hiking cycle. Yet, the FED wasn’t forced to act, as the economy proved resilient.

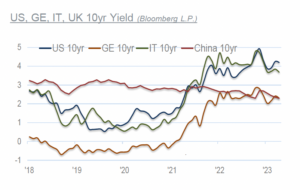

We keep our overweight allocation in fixed income. Judged by the reference US 10yr yield, we see the potential for a tactical rally in bonds. We wouldn’t be surprised to see the 10yr yield back at 3.80%. We stay neutral on high yields and keep our preference for investment grade. Selectivity and diversification is key. We are mindful of the developments in the commodities. What eventually could result in a stagflationary environment.

We keep our overweight allocation in fixed income. Judged by the reference US 10yr yield, we see the potential for a tactical rally in bonds. We wouldn’t be surprised to see the 10yr yield back at 3.80%. We stay neutral on high yields and keep our preference for investment grade. Selectivity and diversification is key. We are mindful of the developments in the commodities. What eventually could result in a stagflationary environment.

S&P500 & Volatility

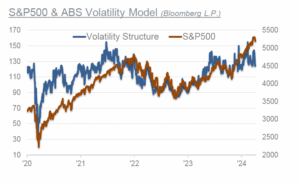

A soft landing is the desirable outcome. We don’t see the macroeconomic situation to be changed a lot in the second quarter. So far, the geopolitical escalations have not had a negative impact on stock markets. Unfortunately, they cannot be ignored either. Consensus expectations for the upcoming US Q1 earnings season call for 5% earnings growth.

What would be half of what was seen during the fourth quarter. There is a good chance the FED can engineer a soft landing. Yet, the FED New York’s recession probability, at 60%, is still much greater than in a typical year. With the turn of the quarter, volatility measures have started to rise. A technical pullback could well occur.

What would be half of what was seen during the fourth quarter. There is a good chance the FED can engineer a soft landing. Yet, the FED New York’s recession probability, at 60%, is still much greater than in a typical year. With the turn of the quarter, volatility measures have started to rise. A technical pullback could well occur.

We favor a neutral allocation in equities. We are overweight on US, neutral on Europe and underweight on China. While there is no historical analogy to the current environment, we focus on high quality and diversification remains key.