GLOBAL STOCK MARKETS

Despite initial hopes that the turbulence of Trump 2.0’s early days would subside, it seems the presidency is continuing its volatile course. With ongoing trade negotiations, FED clashes over interest rates, and significant geopolitical manoeuvres, investors must keep their composure amidst the uncertainty. Q2 continued serving up surprises, making the global investment scene a wild card in April. Trump’s ‘Liberation Day’ tariff policies rocked the markets, spiking volatility measures. On April 9th, markets breathed a sigh of relief as Trump paused tariffs (except for China) for 90 days.

Despite initial hopes that the turbulence of Trump 2.0’s early days would subside, it seems the presidency is continuing its volatile course. With ongoing trade negotiations, FED clashes over interest rates, and significant geopolitical manoeuvres, investors must keep their composure amidst the uncertainty. Q2 continued serving up surprises, making the global investment scene a wild card in April. Trump’s ‘Liberation Day’ tariff policies rocked the markets, spiking volatility measures. On April 9th, markets breathed a sigh of relief as Trump paused tariffs (except for China) for 90 days.

In June, the Israel-Iran conflict took centre stage, driving WTI crude oil prices from $60 to $78, yet market reaction was oddly tame, with volatility metrics only showing minor increases.Jump to July, and tariffs grab headlines again. Five months into Trump 2.0, we see the pace isn’t slowing. The President can change his stance on a dime, leaving investors reeling and strategizing. Critics call it pressure, supporters call it negotiation tactics. Whatever your view, investors must roll with the punches, keeping an eye on underlying macro and microeconomics, while tuning out the policy noise.

As we are at mid-2025, equity and credit markets have bounced back, but geopolitical turbulence and policy volatility continue to shake up the economy. Our global economic outlook remains cautiously optimistic. Tariff uncertainty has split the macro picture, where soft data hints at a downturn, while hard data shows resilience. Households and corporations remain strong, and pauses in tariffs suggested possible negotiations. Markets recovering should boost high-income consumer spending.  Geopolitical tensions pose risks, but the U.S. is more resilient to energy shocks than in the ’70s. We expect slower, positive growth in H2, but risks persist. Surprisingly, US policy might reinvigorate Europe, with Germany’s stimulus potentially doubling growth in 2026-27. China’s outlook is shaky, but pulled-back tariffs in May suggest possible stability. We expect China’s policymakers to provide enough fiscal support to hit their growth target for 2025. Some question US exceptionalism, but America’s advantages—strong demographics, cutting-edge tech, and robust new businesses—should maintain its edge.

Geopolitical tensions pose risks, but the U.S. is more resilient to energy shocks than in the ’70s. We expect slower, positive growth in H2, but risks persist. Surprisingly, US policy might reinvigorate Europe, with Germany’s stimulus potentially doubling growth in 2026-27. China’s outlook is shaky, but pulled-back tariffs in May suggest possible stability. We expect China’s policymakers to provide enough fiscal support to hit their growth target for 2025. Some question US exceptionalism, but America’s advantages—strong demographics, cutting-edge tech, and robust new businesses—should maintain its edge.

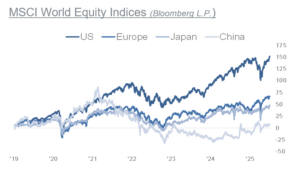

We expected, that 2025 will bring a more balanced development, as valuations and investor sentiment differentials between the US and the rest of the world seemed extreme. We had witnessed a significant rebalancing from US equity markets to Europe and China over the past couple of months. However, following the April lows, US equities have recouped their underperformance. Markets configuration has become stretched again, yet the liquidity backdrop has improved. Deglobalization is not just about trade, people, data, it’s about capital too. In a world of economic nationalism, capital is at risk to deglobalize too. Potentially, one of the big stories of the next few years.

We had witnessed a significant rebalancing from US equity markets to Europe and China over the past couple of months. However, following the April lows, US equities have recouped their underperformance. Markets configuration has become stretched again, yet the liquidity backdrop has improved. Deglobalization is not just about trade, people, data, it’s about capital too. In a world of economic nationalism, capital is at risk to deglobalize too. Potentially, one of the big stories of the next few years.

GLOBAL FIXED INCOME MARKETS

The macro scene has stabilized as fears of a US and EU recession gave way to optimism about potential trade deals. Central banks are nearing the end of their rate-cutting cycles, shifting focus to fiscal policy and debt sustainability. Despite uncertainty, credit markets remained resilient, posting positive returns across sectors and geographies. The Reconciliation Bill in the US intensified debt dynamics concerns. Treasury market experienced a sell-off into May, the US 10yr yield moved above 4.6%. High-deficit countries felt the sell-off.

The macro scene has stabilized as fears of a US and EU recession gave way to optimism about potential trade deals. Central banks are nearing the end of their rate-cutting cycles, shifting focus to fiscal policy and debt sustainability. Despite uncertainty, credit markets remained resilient, posting positive returns across sectors and geographies. The Reconciliation Bill in the US intensified debt dynamics concerns. Treasury market experienced a sell-off into May, the US 10yr yield moved above 4.6%. High-deficit countries felt the sell-off.

Foreign investors’ concerns over the ballooning US deficit and a weakening US Dollar led to selling pressure on US Treasuries.What proved to be only short-lived fears. Major central banks maintained or marginally eased policy rates, with the ECB cutting twice to 2%. The FED held rates steady at its two meetings.

At the June 17-18 meeting it reiterated its wait-and-see mode. In their updated economic forecasts, the FED raised the inflation expectation to 3% from 2.7% at the end of 2025 and marked down their forecast for economic growth to 1.4% from 1.7%, still highlighting the risk of a stagflationary environment. While inflation remains sticky, we expect growth to slow over the coming quarters, paving the way for the FED to deliver two cuts by the end of the year. Yield curves steepened, except in Japan and Canada. President Trump’s ongoing criticism of the Federal Reserve’s reluctance to cut interest rates added to uncertainty. Nonetheless, the FED remains data-dependent, assessing the economic and inflationary impact of Trump’s fiscal policies and import tariffs. Balanced portfolios benefited from bonds’ cushioning effect, as high-yield, corporate, and treasury bonds all provided support and posted positive YTD returns. Interest rates stayed higher than anticipated.

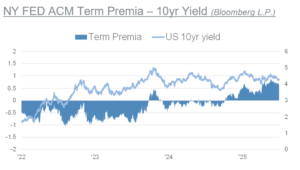

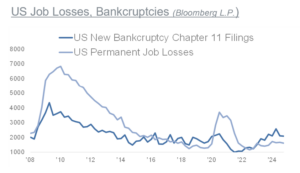

Renewed attention to America’s $36 trillion national debt put the spotlight on government spending in Washington. Recent budget proposals may add $3.3 trillion in deficits over 10 years. Moody’s US credit rating downgrade reflects ongoing concerns about unchecked deficits and rising interest costs, echoing previous fiscal standoffs in 2011, 2013, and 2018-2019. The market has historically bounced back once agreements are reached, underlining the resilience of the US economy. Interestingly, the term premia, a measure that refers to the extra yield investors demand for holding longer-term bonds, continue to remain elevated, reflecting a backdrop of rising issuance and uncertainty.

US DOLLAR

The Dollar has weakened more than 10% this year on concerns about the US economy, including growing warnings over the country’s debt pile. Reports President Trump could pick next FED chair early might have added. In recent years the Dollar has been supported by high US growth compared to the rest of the world,attractive FX carry and strong relative performance of US equities. Calls for de-dollarization in the face of escalating tariff wars are increasing. Although the Dollar’s share of global foreign exchange reserves has declined from over 65% to 59% over the past 10 years, there is no getting around the US capital market and the dominant role of the Dollar in the global reserve system in the foreseeable future.

The Dollar has weakened more than 10% this year on concerns about the US economy, including growing warnings over the country’s debt pile. Reports President Trump could pick next FED chair early might have added. In recent years the Dollar has been supported by high US growth compared to the rest of the world,attractive FX carry and strong relative performance of US equities. Calls for de-dollarization in the face of escalating tariff wars are increasing. Although the Dollar’s share of global foreign exchange reserves has declined from over 65% to 59% over the past 10 years, there is no getting around the US capital market and the dominant role of the Dollar in the global reserve system in the foreseeable future.

In our view, the correction of the Dollar since February is close to being exhausted, as the bearishness has reached extreme. With the seismic shift in global trade underway, geopolitical uncertainties and the different approaches to public finances, great macro trade opportunities are coming up in forex markets.

COMMODITIES

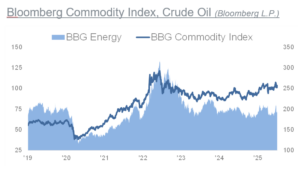

The Bloomberg Commodity Index declined in the quarter. The energy component was weak. The agriculture component was also down, although cocoa surged higher.

Livestock, industrial metals and precious metals advanced. Elevated levels of risk, such as trade tariffs and geopolitical concerns, continue to see investors favour the safe haven of precious metals. Escalating conflict risk in the Middle East caused a brief oil price surge amid worries about disruption to shipping, but oversupply of oil kept prices contained. OPEC+ announced a higher-than-expected increase in oil production for August of 548k bpd, after it had announced to gradually increase production by 411k bpd for May, June and July. Despite the geopolitical risks, the Israel-Iran truce has lowered the geopolitical premium and a higher-than-expected output hike from OPEC+ is threatening to push the oil market into a sizable surplus by year-end.

We keep the recommended tactical allocation in commodities at neutral. We remain strategically positive on precious metals. Further, it’s worth to bear in mind, that commodities as a group comprise less than 2% of total global assets under management. It’s a vastly under-owned cohort.

MACRO

Market based inflation expectations, which are important to monitor, have stayed closer to 2% for most part since the beginning of 2021. The disinflationary forces have been playing out and inflation data have slowed significantly from their 2022 peaks. US headline inflation fell to as low as 2.3% y/y in April.

However, tariffs should start to show up more visibly in the data in the coming months. The setup of tariffs, firm inventories, and CPI methodology all lead to a delayed pass-through into the official consumer price measure. The FED’s preferred inflation gauge, PCE, was reported 2.7% for May. This proves the stickiness of inflation above the 2% target. We have pointed out in previous reports that a post-peak globalization world will exhibit stagflationary tendencies. That growth will be lower than inflation.In the latest tariff developments, following the 90 day pause, it appears tariffs are going up, not down. The US Administration has sent letters to 24 countries and the EU with new tariffs to kick in August 1. For Brazil, 50%, and the EU, 30%, the rates are notably higher.

This comes on the back of an already slowing US economy, while the scale of tariffs has taken markets again by surprise. Stagflation risks are rising, as the tariffs will lower US growth and raise prices substantially. There is the risk, the market is underestimating the negative economic impact from tariffs.

This comes on the back of an already slowing US economy, while the scale of tariffs has taken markets again by surprise. Stagflation risks are rising, as the tariffs will lower US growth and raise prices substantially. There is the risk, the market is underestimating the negative economic impact from tariffs.

On the other hand, investors must closely watch China and its monetary policy actions. Chinese liquidity is on the up, helped by the weak US Dollar and underpinned by a need to support the stuttering real economy.

While the FED influences financial markets, the PBoC drives real economy and commodity cycles. We live in a debt-dominated world. Today, financial markets serve as debt refinancing mechanism, more so than as a capital raising vehicles for new investments.

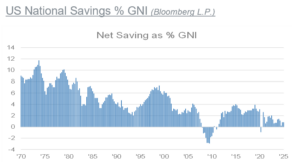

US government debt has risen nine times since 2000, gold has risen by the same pace. However, the debt problem is not unique to the US. Volatility can interrupt the delicate debt-refinancing process that dominates the financial markets.

In 2025 the first of the maturity walls will be faced, when a significant volume of debt is scheduled to mature, necessitating refinancing or repayment by the issuers. A large part pertains to 5 year bonds issued in 2020 during the pandemic, which were secured at low-interest rates. In addition to that, the US Treasury needs to refinance 25% of the outstanding debt, approximately 9tn. From that perspective, one might be intrigued to guess, that the Trump administration could welcome an economic slowdown, to bring down interest rates. At any rate, the tariff wars show, it is important to understand, that a fundamental reorganization of the global economy along with its supply chains, energy systems and underlying technology foundations is taking place.

TACTICAL ALLOCATION

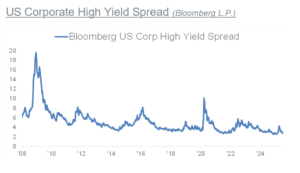

The inflationary forces are structural and secular, on higher debt-load, demographics and on-shoring of manufacturing. We have been in an interim period for the past two and half years. Inflation risks have picked up by the end of 2024. The market currently prices in 50 bp cut by the FED for 2025, and sees the ECB at the terminal rate. Analysts on average expect the US 10year yield to close 2025 at 4.29%, up from 4.16% at the end of 2024. We recommend a neutral allocation in fixed income. We prefer investment grade. We upgrade high yield to neutral, as recession fears recede. Although credit spreads have tightened a lot, probably too much. However, current market conditions are favorable, with yields around 6%, compared to 4% three years ago. Selectivity and diversification are key. We are mindful of the developments in the commodities, for signs, should inflation risks accentuate.

The inflationary forces are structural and secular, on higher debt-load, demographics and on-shoring of manufacturing. We have been in an interim period for the past two and half years. Inflation risks have picked up by the end of 2024. The market currently prices in 50 bp cut by the FED for 2025, and sees the ECB at the terminal rate. Analysts on average expect the US 10year yield to close 2025 at 4.29%, up from 4.16% at the end of 2024. We recommend a neutral allocation in fixed income. We prefer investment grade. We upgrade high yield to neutral, as recession fears recede. Although credit spreads have tightened a lot, probably too much. However, current market conditions are favorable, with yields around 6%, compared to 4% three years ago. Selectivity and diversification are key. We are mindful of the developments in the commodities, for signs, should inflation risks accentuate.

S&P500 & Volatility

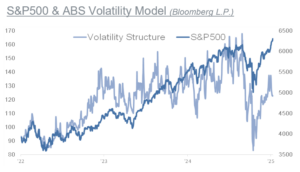

The upswing in the investment cycle maybe 34 months old, if one counts from the low in October 2022, when the current liquidity cycle got started. But the investment climate is still risk on. Asset allocation today is primarily driven by global liquidity. What is increasingly the result of government spending, respectively what can be termed fiscal dominance. It can be expected that China and other economies will likely fight the recessionary forces. The FED so far seems reluctant to re-engage in stimulus, via a larger balance sheet and QE. However, monetary inflation will probably force the FED to step in. Equity valuations are not cheap, with the forward 12-month P/E ratio for the S&P500 at 22.3, compared to the 5-year average of 19.9. However, investor positioning is still rather cautious. We upgrade the allocation in equities to neutral, but remain vigilant. Things can change day-to-day. We are neutral on US, Europe and China, while maintaining the underweight on Japan. We focus on high quality and diversification remains key.

The upswing in the investment cycle maybe 34 months old, if one counts from the low in October 2022, when the current liquidity cycle got started. But the investment climate is still risk on. Asset allocation today is primarily driven by global liquidity. What is increasingly the result of government spending, respectively what can be termed fiscal dominance. It can be expected that China and other economies will likely fight the recessionary forces. The FED so far seems reluctant to re-engage in stimulus, via a larger balance sheet and QE. However, monetary inflation will probably force the FED to step in. Equity valuations are not cheap, with the forward 12-month P/E ratio for the S&P500 at 22.3, compared to the 5-year average of 19.9. However, investor positioning is still rather cautious. We upgrade the allocation in equities to neutral, but remain vigilant. Things can change day-to-day. We are neutral on US, Europe and China, while maintaining the underweight on Japan. We focus on high quality and diversification remains key.