GLOBAL STOCK MARKETS

The most talked-about issue in global financial markets and economics were the Trump administration’s tariff announcements. With the administration arguing that tariffs are a tool to make America a manufacturing superpower again. While most economists disagreed and argued, that tariffs were bad for consumers and ultimately the global economy. Tariffs are an old concept, used as taxes on foreign goods and services, to shield domestic producers from competition from foreigners. Tariffs increase the costs for consumers. The downside in a globalized world is, there is no company producing goods with inputs that are only of domestic origin. Countries respond to Trump’s tariffs by implementing their own tariffs. What in turn threatens American exporters.

The FED thinks, that tariffs might increase inflation in the near term, it sees it as transitory. There will be a period of high inflation and lower growth. Yet, without monetary expansion, economic actors face budget constraints. The inflicted economic slowdown, that the tariffs create, will lead to more federal debt and money printing. Important will be, for how long the new tariffs will stay, or if they are just meant as a negotiating tool for Trump. It’s clear, tariffs increase economic unpredictability and create financial uncertainty. There will be a rise in overall market volatility. The first quarter was a rollercoaster ride.

The FED thinks, that tariffs might increase inflation in the near term, it sees it as transitory. There will be a period of high inflation and lower growth. Yet, without monetary expansion, economic actors face budget constraints. The inflicted economic slowdown, that the tariffs create, will lead to more federal debt and money printing. Important will be, for how long the new tariffs will stay, or if they are just meant as a negotiating tool for Trump. It’s clear, tariffs increase economic unpredictability and create financial uncertainty. There will be a rise in overall market volatility. The first quarter was a rollercoaster ride.

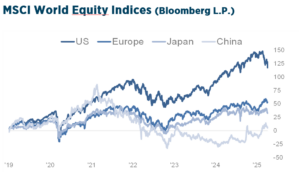

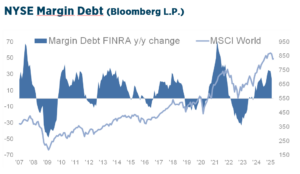

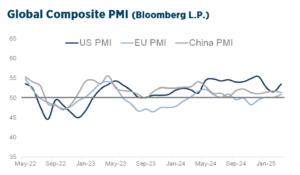

The start into the new year was bumpy, before the three major US indices reached new all-time highs in February. Macroeconomic concerns started to become more prominent, with inflation figures and weak consumer confidence hurting domestic sentiment. The technology breakthrough made by Chinese AI DeepSeek raised questions about the dominance of the AI giants in the US market. This led to a significant sell-off in the mega cap tech stocks. Europe has been pushed to review its defence policies, as US military support has become less reliable. The German parliament has voted in favour of a huge fiscal package and changes to the debt brake. Which can be described as a historic turning point in German fiscal policy. While Europe is engaging in fiscal stimulus, the US is actively cutting federal spending. We expected, that 2025 will bring a more balanced development, as valuations and investor sentiment differentials between the US and the rest of the world seemed extreme.We have witnessed a significant rebalancing from US equities to Europe and China over the past couple of months. That volatility returns with such vengeance surprised most people. Markets configuration had become stretched, as the liquidity backdrop had weakened since the start of the year. The sell-off over the turn of the quarter, intensified by the April 2 tariffs has all the hallmarks of a liquidity event. Deglobalization is not just about trade, people, data, it’s about capital too. In a world of economic nationalism, capital is at risk to deglobalize too. Potentially, one of the big stories of the next few years.

We expected, that 2025 will bring a more balanced development, as valuations and investor sentiment differentials between the US and the rest of the world seemed extreme.We have witnessed a significant rebalancing from US equities to Europe and China over the past couple of months. That volatility returns with such vengeance surprised most people. Markets configuration had become stretched, as the liquidity backdrop had weakened since the start of the year. The sell-off over the turn of the quarter, intensified by the April 2 tariffs has all the hallmarks of a liquidity event. Deglobalization is not just about trade, people, data, it’s about capital too. In a world of economic nationalism, capital is at risk to deglobalize too. Potentially, one of the big stories of the next few years.

GLOBAL FIXED INCOME MARKETS

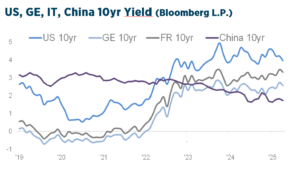

Global macroeconomic developments in the first quarter were significant. The concept of US exceptionalism was called into question, as increased policy uncertainty contributed to a decline in sentiment and growing concerns about a potential recession. In contrast, Germany’s shift in its fiscal regime had a marked impact on Europe’s outlook, causing a stark divergence in fixed income markets. In March, Germany’s parliament passed incoming Chancellor Merz’s plans to ease borrowing restrictions, excluding defence and security spending from the country’s stringent debt regulations. This decision enables the creation of a €500 billion infrastructure fund to operate over the next 12 years. As a result, German Bunds experienced the most significant sell-off across the Eurozone, with yields recording their largest daily jump since the country’s reunification in 1990. Whereas the EU is prioritizing fiscal expansion, the US is prioritizing reduction of the 7% fiscal deficit. Initially, this is coming from reduced spending, what is growth negative.

Global macroeconomic developments in the first quarter were significant. The concept of US exceptionalism was called into question, as increased policy uncertainty contributed to a decline in sentiment and growing concerns about a potential recession. In contrast, Germany’s shift in its fiscal regime had a marked impact on Europe’s outlook, causing a stark divergence in fixed income markets. In March, Germany’s parliament passed incoming Chancellor Merz’s plans to ease borrowing restrictions, excluding defence and security spending from the country’s stringent debt regulations. This decision enables the creation of a €500 billion infrastructure fund to operate over the next 12 years. As a result, German Bunds experienced the most significant sell-off across the Eurozone, with yields recording their largest daily jump since the country’s reunification in 1990. Whereas the EU is prioritizing fiscal expansion, the US is prioritizing reduction of the 7% fiscal deficit. Initially, this is coming from reduced spending, what is growth negative.

Although the hopes are, that growth would come from deregulation and tax cuts. US Treasuries demonstrated strong performance.

Although the hopes are, that growth would come from deregulation and tax cuts. US Treasuries demonstrated strong performance.

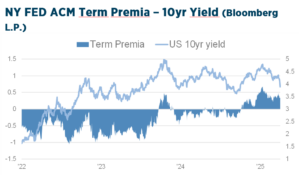

The turn of the quarter was notable, disappointing consumer reports and sharply falling stock markets led to a flight to safety and briefly brought the US 10yr yield under 4%. The fall in US bond yields are the result of collapsing policy rate expectations, on growth worries. Interestingly, the term premia, a recent key driver of yields, however, continues to point upwards, reflecting a backdrop of rising issuance and uncertainty. The 10r German yields rose from 2.37% to 2.74% at the end of the quarter. Notable divergence was also observed in corporate bond markets. US Dollar-denominated bonds exhibited superior performance to Euro bonds across both investment-grade and high-yield markets.

Japanese government bonds underperformed, as yields surged in response to strong Q4 GDP growth of 2.2% and rising inflation levels. On the other hand, China’s predominantly deflationary outlook served to mitigate the increase in yields. The FED held rates steady at 4.25-4.50% in Q1. At the March meeting, the FED’s Summary of Economic Projections downgraded 2025 GDP growth to 1.7% from 2.1% and core PCE inflation was revised up to 2.8% form 2.5%, signalling rising stagflation risks. This uncomfortable mix of economic data underscores the challenging balancing act ahead for the FED. The ECB lowered its key interest rates twice by 25bp, bringing the main refinancing rate to 2.65%. The ECB staff macroeconomic projections lowered 2025 GDP to 0.9% form 1.1% and increased Euro area CPI to 2.3% from an initial 2.1%.

Japanese government bonds underperformed, as yields surged in response to strong Q4 GDP growth of 2.2% and rising inflation levels. On the other hand, China’s predominantly deflationary outlook served to mitigate the increase in yields. The FED held rates steady at 4.25-4.50% in Q1. At the March meeting, the FED’s Summary of Economic Projections downgraded 2025 GDP growth to 1.7% from 2.1% and core PCE inflation was revised up to 2.8% form 2.5%, signalling rising stagflation risks. This uncomfortable mix of economic data underscores the challenging balancing act ahead for the FED. The ECB lowered its key interest rates twice by 25bp, bringing the main refinancing rate to 2.65%. The ECB staff macroeconomic projections lowered 2025 GDP to 0.9% form 1.1% and increased Euro area CPI to 2.3% from an initial 2.1%.

US DOLLAR

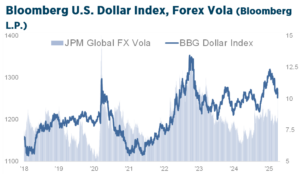

The Dollar had continued its upward trajectory from the fourth quarter. The Bloomberg Dollar Index moved 9% higher during this period. The back and forth of tariff announcements and postponements led to a reversal. Reports of Trump-Putin peace talks sent the Euro higher, which had traded as low as 1.0140 to the USD in early February. The anticipated historic increase in German fiscal spending, along with growing concerns about the negative impact of aggressive tariffs on the US economy accelerated things. In recent years the Dollar has been supported by high US growth compared to the rest of the world, attractive FX carry and strong relative performance of US equities. At this stage, a convergence of growth rates between the US and the other G10 countries seems to be the most likely medium-term scenario.

The Dollar had continued its upward trajectory from the fourth quarter. The Bloomberg Dollar Index moved 9% higher during this period. The back and forth of tariff announcements and postponements led to a reversal. Reports of Trump-Putin peace talks sent the Euro higher, which had traded as low as 1.0140 to the USD in early February. The anticipated historic increase in German fiscal spending, along with growing concerns about the negative impact of aggressive tariffs on the US economy accelerated things. In recent years the Dollar has been supported by high US growth compared to the rest of the world, attractive FX carry and strong relative performance of US equities. At this stage, a convergence of growth rates between the US and the other G10 countries seems to be the most likely medium-term scenario.  Calls for de-dollarization in the face of escalating tariff wars are increasing. Although the dollar’s share of global foreign exchange reserves has declined from over 65% to 59% over the past 10 year, there is no getting around the US capital market and the dominant role of the Dollar in the global reserve system in the foreseeable future. However, with the seismic shift in global trade underway, geopolitical uncertainties and the different approaches to public finances, great macro trade opportunities are opening up.

Calls for de-dollarization in the face of escalating tariff wars are increasing. Although the dollar’s share of global foreign exchange reserves has declined from over 65% to 59% over the past 10 year, there is no getting around the US capital market and the dominant role of the Dollar in the global reserve system in the foreseeable future. However, with the seismic shift in global trade underway, geopolitical uncertainties and the different approaches to public finances, great macro trade opportunities are opening up.

COMMODITIES

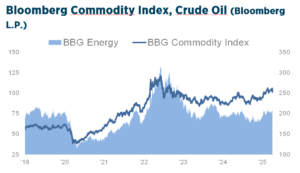

The Bloomberg Commodity Index was +8.8% on the quarter, with all sub-indices showing positive returns. Precious metals were the strongest component of the index, up 18%, while agricultures, after initials gains, were lagging, +2%. Gold is the top performing assets over the past 12 months, +39%. Gold’s share in global FX-reserves has increased in the past ten years, from 10% to over 15%. In a surprise move, OPEC+ decided to hike supply by 411k bpd in May, following a first hike of 138k in April. The organisation cited “continuing healthy market fundamentals and the positive market outlook” and added that “the gradual increases may be paused or reversed subject to evolving market conditions.” The surprise output hike is probably politically motivated. Longer-term, AI’s growing demand for power, will add to the investment case for key metals.

The Bloomberg Commodity Index was +8.8% on the quarter, with all sub-indices showing positive returns. Precious metals were the strongest component of the index, up 18%, while agricultures, after initials gains, were lagging, +2%. Gold is the top performing assets over the past 12 months, +39%. Gold’s share in global FX-reserves has increased in the past ten years, from 10% to over 15%. In a surprise move, OPEC+ decided to hike supply by 411k bpd in May, following a first hike of 138k in April. The organisation cited “continuing healthy market fundamentals and the positive market outlook” and added that “the gradual increases may be paused or reversed subject to evolving market conditions.” The surprise output hike is probably politically motivated. Longer-term, AI’s growing demand for power, will add to the investment case for key metals.  Whether copper for grid expansions and upgrades, or uranium to meet growing low-carbon energy needs. We keep the recommended tactical allocation in commodities at neutral. We remain strategically positive on precious metals. Further, it’s worth to bear in mind, that commodities as a group comprise less than 2% of total global assets under management. It’s a vastly under-owned cohort.

Whether copper for grid expansions and upgrades, or uranium to meet growing low-carbon energy needs. We keep the recommended tactical allocation in commodities at neutral. We remain strategically positive on precious metals. Further, it’s worth to bear in mind, that commodities as a group comprise less than 2% of total global assets under management. It’s a vastly under-owned cohort.

MACRO

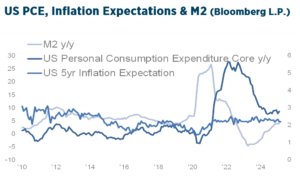

Market-based inflation expectations, which are important to monitor, have stayed closer to 2% for most part since the beginning of 2021. The disinflationary forces have been playing out and inflation data have slowed significantly from their 2022 peaks. US headline inflation has fallen to as low as 2.4% y/y in September, however was at 2.8% in February. The FED’s preferred gauge, PCE, has fallen to as low as 2.6% in June,it was reported 2.8% for February as well. This proves the stickiness of inflation above the 2% target. We have pointed out in previous reports that a post-peak globalization world will exhibit stagflationary tendencies.

Market-based inflation expectations, which are important to monitor, have stayed closer to 2% for most part since the beginning of 2021. The disinflationary forces have been playing out and inflation data have slowed significantly from their 2022 peaks. US headline inflation has fallen to as low as 2.4% y/y in September, however was at 2.8% in February. The FED’s preferred gauge, PCE, has fallen to as low as 2.6% in June,it was reported 2.8% for February as well. This proves the stickiness of inflation above the 2% target. We have pointed out in previous reports that a post-peak globalization world will exhibit stagflationary tendencies.

That growth will be lower than inflation. US President Trump announced tariffs of an unexpectedly high magnitude. In addition to a comprehensive import tariff of 10%, higher tariffs will come into effect for over 50 countries. This comes on the back of an already slowing US economy, while the scale of tariffs has taken markets by surprise. Stagflation risks are rising, as the tariffs will lower US growth and raise prices substantially.

Key will be, that the US government addresses market and business concerns, so confidence could partially rebound. In an ideal world, the US government would outline a negotiation path and clarify its intentions for using tariff revenues to reduce corporate taxes. We live in a debt-dominated world.

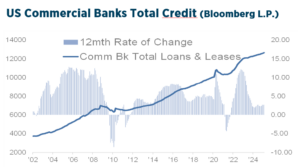

Today, financial markets serve as debt refinancing mechanism, more so than as a capital raising vehicles for new investments. US government debt has risen nine times since 2000, gold has risen by the same pace. However, the debt problem is not unique to the US. Volatility can interrupt the delicate debt-refinancing process that dominates the financial markets. In 2025 the first of the maturity walls will be faced, when a significant volume of debt is scheduled to mature, necessitating refinancing or repayment by the issuers.A large part pertains to 5 year bonds issued in 2020 during the pandemic, which were secured at low-interest rates.

In addition to that, the US Treasury needs to refinance 25% of the outstanding debt, approximately $9tn. From that perspective, one might be intrigued to guess, that the Trump administration could welcome an economic slowdown, to bring down interest rates. At any rate, the tariff wars show, it’s important to understand, that a fundamental reorganization of the global economy along with its supply chains, energy systems and underlying technology foundations is taking place.

TACTICAL ALLOCATION

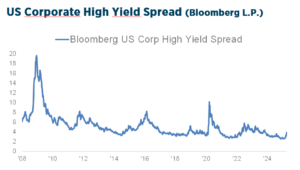

The inflationary forces are structural and secular, on higher debt-load, demographics and on-shoring of manufacturing. We have been in an interim period for the past two years. Inflation risks have picked up at end of 2024. After the recent turmoil, the market currently prices in 75 bp cut by the FED for 2025, and a total of 50 bp cuts by the ECB. Analysts on average expect the US 10year yield to close 2025 at 4.26%, up from 4.16% at the end of 2024. We recommend a neutral allocation in fixed income. We prefer investment grade. We cut high yield to underweight, as the economic slowdown will reverberate through the credit markets. Selectivity and diversification are key. We are mindful of the developments in the commodities, for signs, should inflation risks accentuate.

The inflationary forces are structural and secular, on higher debt-load, demographics and on-shoring of manufacturing. We have been in an interim period for the past two years. Inflation risks have picked up at end of 2024. After the recent turmoil, the market currently prices in 75 bp cut by the FED for 2025, and a total of 50 bp cuts by the ECB. Analysts on average expect the US 10year yield to close 2025 at 4.26%, up from 4.16% at the end of 2024. We recommend a neutral allocation in fixed income. We prefer investment grade. We cut high yield to underweight, as the economic slowdown will reverberate through the credit markets. Selectivity and diversification are key. We are mindful of the developments in the commodities, for signs, should inflation risks accentuate.

S&P500 & VOLATILITY

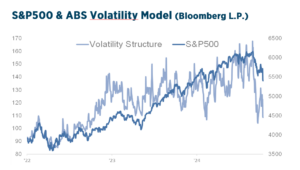

Comparisons are drawn to the 1930s. However, back then it was a severe monetary deflation. It can be expected that China and other economies will likely fight the recessionary forces. The FED so far seems reluctant to re-engage in stimulus, via a larger balance sheet and QE. However, monetary inflation will probably force the FED to step in. Since everything is currently in flux, it is difficult to quantify the economic slowdown. US stocks earnings will decline, as analyst estimates have begun to reflect this, with consensus calling for the S&P500 to earn $266.70 per share in 2025, down from $272.15 at the end of last year. It appears likely that this figure will experience a further decline as the complete effects of tariffs and the widespread ambiguities become evident. We cut the allocation in equities to neutral/underweight amid the increased uncertainty on the various fronts. Things can change day-to-day. We are neutral on US, Europe and China, while maintaining the underweight on Japan. We focus on high quality and diversification remains key.