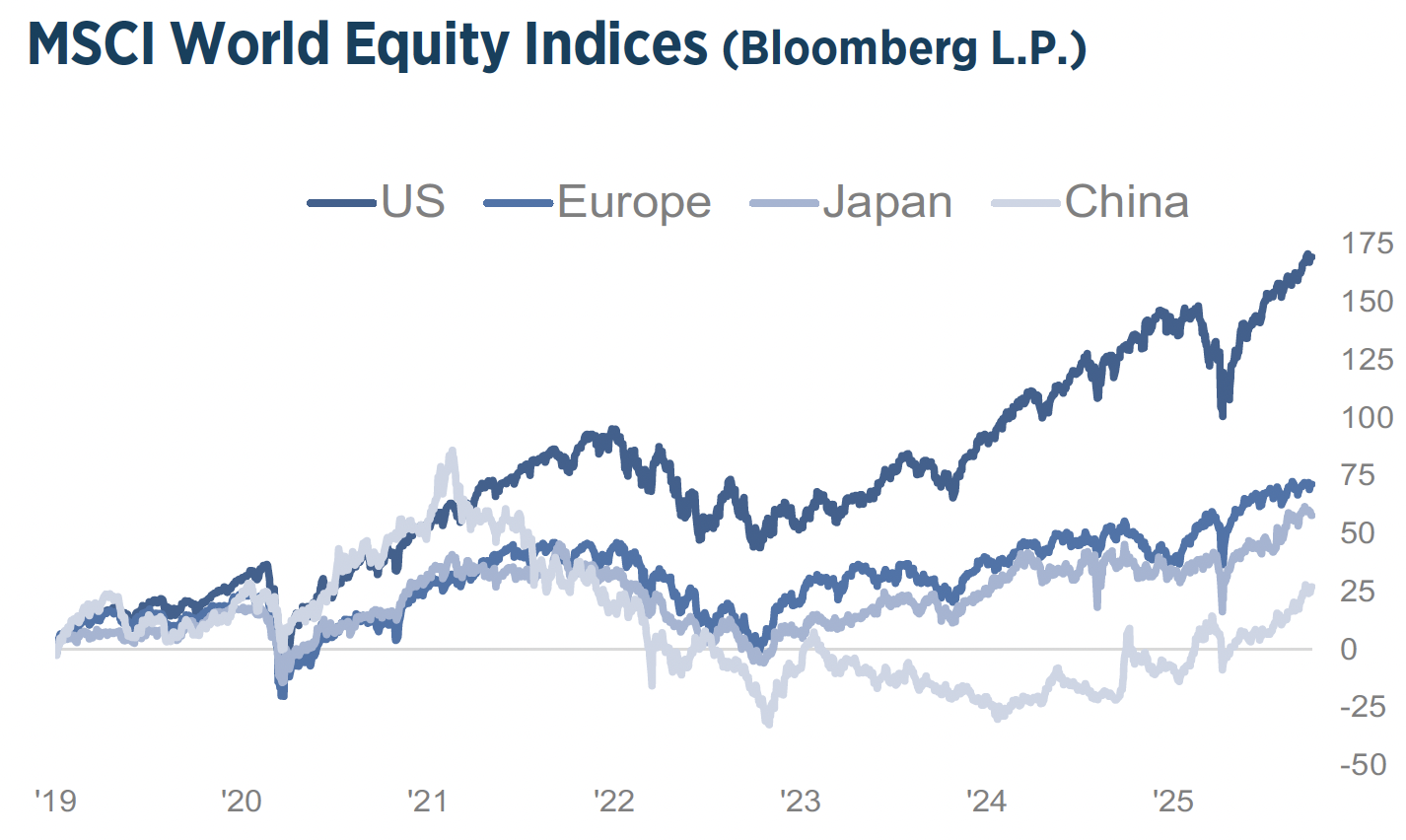

GLOBAL STOCK MARKETS

In the third quarter macroeconomic developments were back in focus, after US labor market data has weakened considerably. The 5-month average Nonfarm Payrolls dropped to 53k created jobs in August, down from 197k in January. In addition, the preliminary benchmark revisions showed 911k less jobs created than previously reported for the 12 months ending in March 2025. The third estimate of GDP for Q2 was significantly revised up to 3.8% from3.3%, primarily reflecting a decrease in imports and an increase in consumer spending. Core PCE inflation for 2024 was revised higher. 4Q24 was running at 3% vs 2.8% previously reported. With effect from October 1, the Trump administration announced the largest wave of tariff announcements in months, such as 100% tariff on pharmaceuticals.

In the third quarter macroeconomic developments were back in focus, after US labor market data has weakened considerably. The 5-month average Nonfarm Payrolls dropped to 53k created jobs in August, down from 197k in January. In addition, the preliminary benchmark revisions showed 911k less jobs created than previously reported for the 12 months ending in March 2025. The third estimate of GDP for Q2 was significantly revised up to 3.8% from3.3%, primarily reflecting a decrease in imports and an increase in consumer spending. Core PCE inflation for 2024 was revised higher. 4Q24 was running at 3% vs 2.8% previously reported. With effect from October 1, the Trump administration announced the largest wave of tariff announcements in months, such as 100% tariff on pharmaceuticals.

On the same day, the US government shut down for the first time in nearly seven years, halting operations across multiple departments and agencies, as Republicans and Democrats failed to break a deadlock over Obamacare health funding. Global stocks continued to rise, led by US and Chinese stocks, whereas European markets stagnated. The mania for AI related stocks remained the main driver of the markets advance, with new tech leaders emerging outside the Magnificent 7. The US stock market has risen 40% since the April 7 low, following President Trump’s tariff announcements shock, brushing aside worries about high stock prices, unclear government policies, and the effects of tariffs. Nvidia reached a milestone in July, becoming the first company to surpass a market capitalization of $4 trillion.

With the S&P500 at a new record high, the valuation has become more expensive, trading at a forward P/E of 23x, with slowing growth expectations. While valuations have historically been a poor market-timing tool, but it can be seen as a sign of building euphoria, compounding worries around the concentration of big tech names. On the other hand, Chinese stocks are still attractively valued, yet, have been the outstanding performer this year. Many believed, that China would be the main loser in the trade war, however, the Trump administration has been rather cautious in dealing with China, as it’s in an advantageous position because of considerable control over rare earths.

With the S&P500 at a new record high, the valuation has become more expensive, trading at a forward P/E of 23x, with slowing growth expectations. While valuations have historically been a poor market-timing tool, but it can be seen as a sign of building euphoria, compounding worries around the concentration of big tech names. On the other hand, Chinese stocks are still attractively valued, yet, have been the outstanding performer this year. Many believed, that China would be the main loser in the trade war, however, the Trump administration has been rather cautious in dealing with China, as it’s in an advantageous position because of considerable control over rare earths.

Still dealing with the aftermath of the real estate crisis, Chinese authorities have strongly supported the buildup of a competitive domestic technology sector. It has become clear, that Chinese tech companies are gaining strength in the AI space. Overall, the picture in 2025 has been marked by labor market cracks, fiscal deterioration and tariff shocks. Equity markets have stayed buoyant due to AI-driven tech, but structural risks, inflation, deficits, FED independence and geopolitical frictions remain elevated. We believe equity markets are in a positive but delicate equilibrium, they can continue to go higher, but are increasingly sensitive to a broad range of macro and political factors.

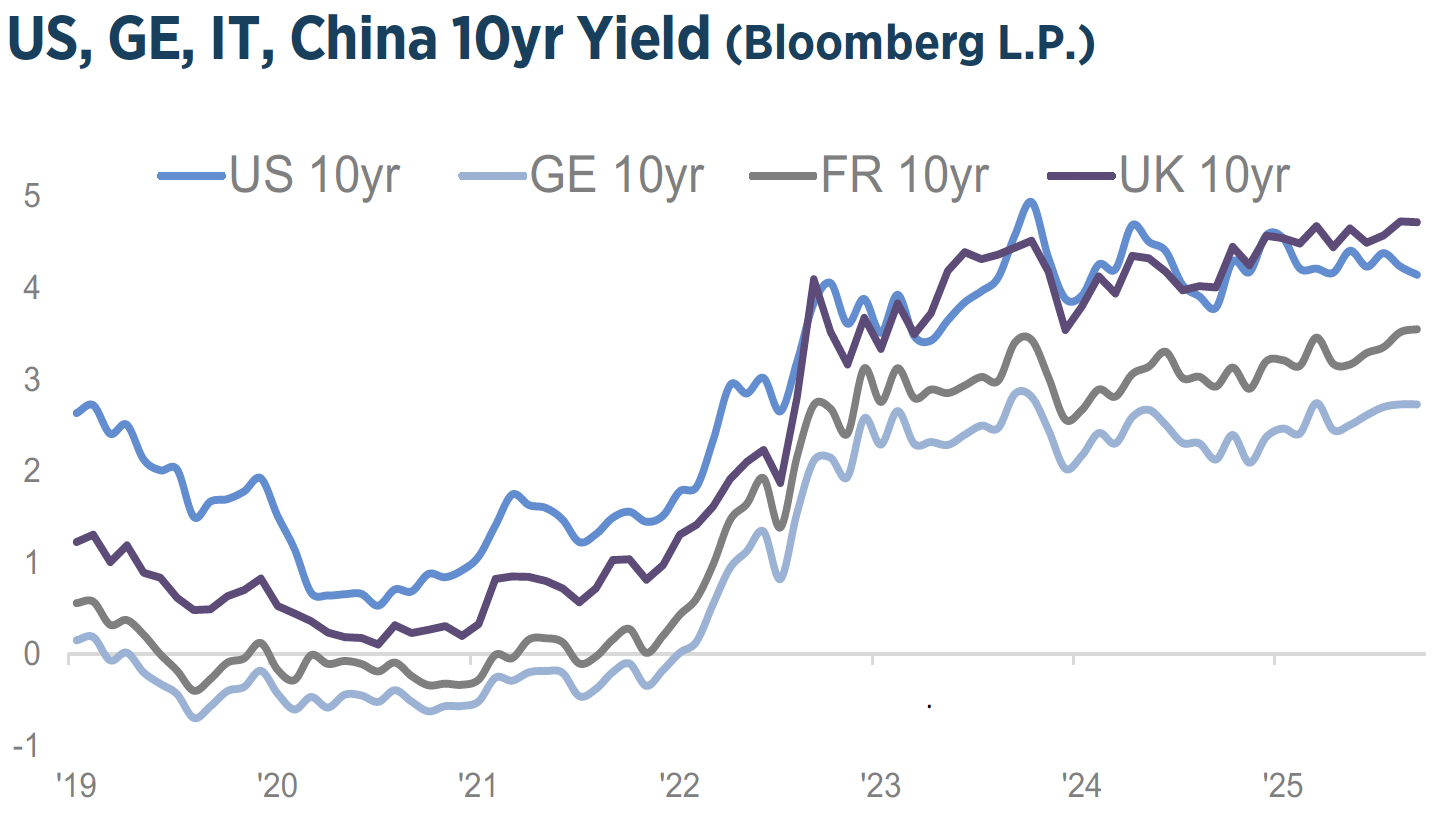

GLOBAL FIXED INCOME MARKETS

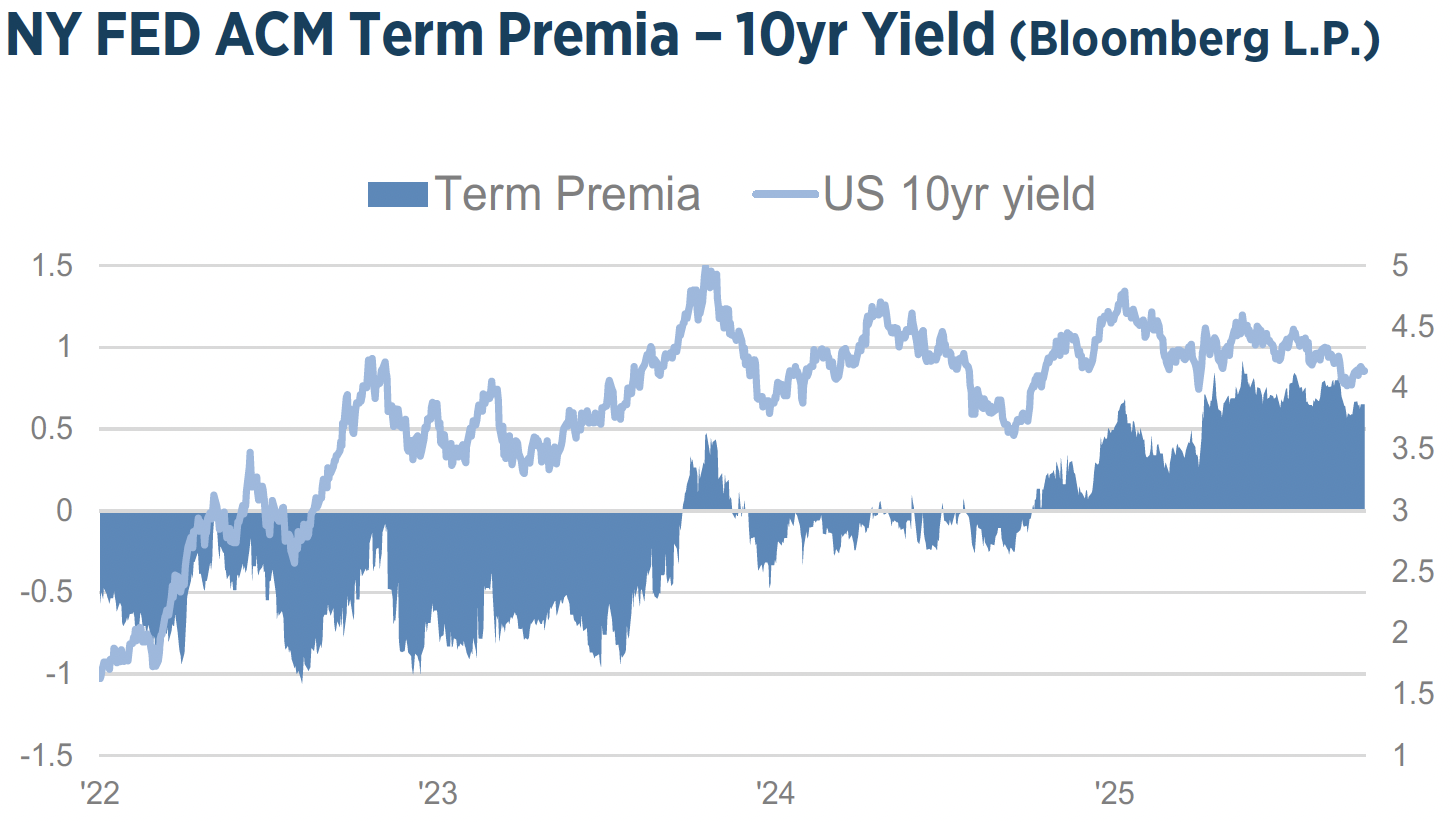

Global bond yields behaved mixed in Q3. Long-term bond yields rose in Europe and Japan, while the benchmark US 10yr yield fell 8bps to 4.15%. Interestingly, the term premia, a measure that refers to the extra yield investors demand for holding longer-term bonds, continue to remain elevated, reflecting a backdrop of rising issuance and uncertainties. Overseas investors returned to purchase US Treasuries. Concerns that underlying geopolitical tensions would cause foreigners to stop purchasing, or even sell, US government debt have yet to materialize.

Global bond yields behaved mixed in Q3. Long-term bond yields rose in Europe and Japan, while the benchmark US 10yr yield fell 8bps to 4.15%. Interestingly, the term premia, a measure that refers to the extra yield investors demand for holding longer-term bonds, continue to remain elevated, reflecting a backdrop of rising issuance and uncertainties. Overseas investors returned to purchase US Treasuries. Concerns that underlying geopolitical tensions would cause foreigners to stop purchasing, or even sell, US government debt have yet to materialize.

The Bloomberg Global Aggregate Bond Index was +0.6% in Q3, US Treasuries +1.5%, whereas European Government Bonds fell -0.2%, on political uncertainties and fiscal worries. French 10yr yield surpassed those of Italy, as France faced a fresh political crisis. UK’s 10yr yield trade way above, as the budget debate is under way.

Speculation arose, whether the IMF will step in, as it happened in the UK in 1976. In light of the weak jobs market, the FED expectedly lowered key rates by 25bps, yet warning inflation remains somewhat elevated. The FED expects inflation ending this year at 3% and economic growth to be at 1.6%. The ECB kept interest rates unchanged, while projecting inflation to be 2.1% and growth at 1.2%. The FED, as always, was particularly in focus. At the Jackson Hole Symposium in August FED Chair Powell pointedly kept the door open to a near-term rate cut, what markets read as a dovish pivot. Powell emphasized softer labor-market conditions and a shift in the balance of risks.

President Trump has repeatedly publicly called on the FED to cut rates faster and more aggressively than the FED’s prevailing view. Trump tried to fire FED Governor Lisa Cook, what triggered legal challenges and court interventions, raising questions about the FED’s independence. Just ahead of the September FED meeting, White House economic adviser, Stephen Miran, was confirmed to the FED board. His dual role and past alignment with Trump reinforced concerns about political influence. Despite the pressure from the White House for larger cuts, the FED decided in an 11-1 decision to reduce only by 25bps. That no other governor dissented was a significant message. Another surprise came from the wide dispersion in the ‘Dot Plot’, the governors individual rate projections, showing how divided the FED is on how fast to cut rates. With a spread of 125bps between the low and high estimate for 2026, incoming economic data will be scrutinized.

US DOLLAR

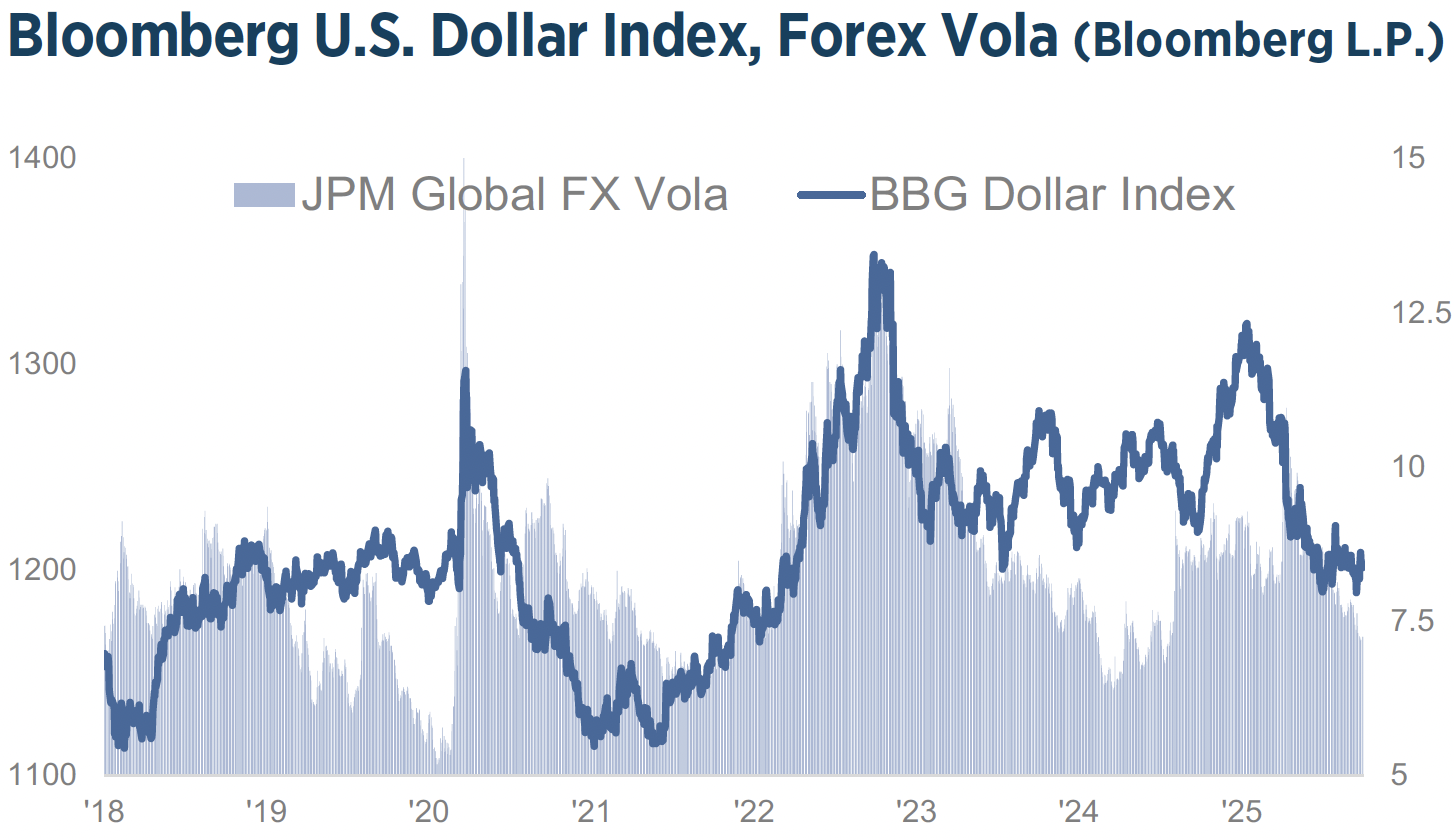

The Dollar has fallen 10% from its peak in early February. Calls for de-dollarization in the face of escalating tariff wars were increasing. Many saw the end of the US Dollar as a reserve currency and safe haven. However, one cannot exclude the possibility that the US Administration wants to weaponize the US Dollar and so make it weaker to improve industrial competitiveness. Yet, capital inflows into US asset remain. Although the Dollar’s share of global foreign exchange reserves has declined from over 65% to 58% over the past 10 years, there is no getting around the US capital market and the dominant role of the Dollar in the global reserve system in the foreseeable future.

The Dollar has fallen 10% from its peak in early February. Calls for de-dollarization in the face of escalating tariff wars were increasing. Many saw the end of the US Dollar as a reserve currency and safe haven. However, one cannot exclude the possibility that the US Administration wants to weaponize the US Dollar and so make it weaker to improve industrial competitiveness. Yet, capital inflows into US asset remain. Although the Dollar’s share of global foreign exchange reserves has declined from over 65% to 58% over the past 10 years, there is no getting around the US capital market and the dominant role of the Dollar in the global reserve system in the foreseeable future.

The launch and growth of stablecoins generally increase demand for US Dollars. Over 90% of the stablecoin market is backed 1:1 by US Dollar assets, such as Treasury bills. We reiterate our assessment from late June that the Dollar correction has likely reached its limits. It should be recalled, that significant macro trading opportunities are emerging in the FX markets due to the current upheavals in global trade, geopolitical uncertainties, and diverging approaches to public finances.

COMMODITIES

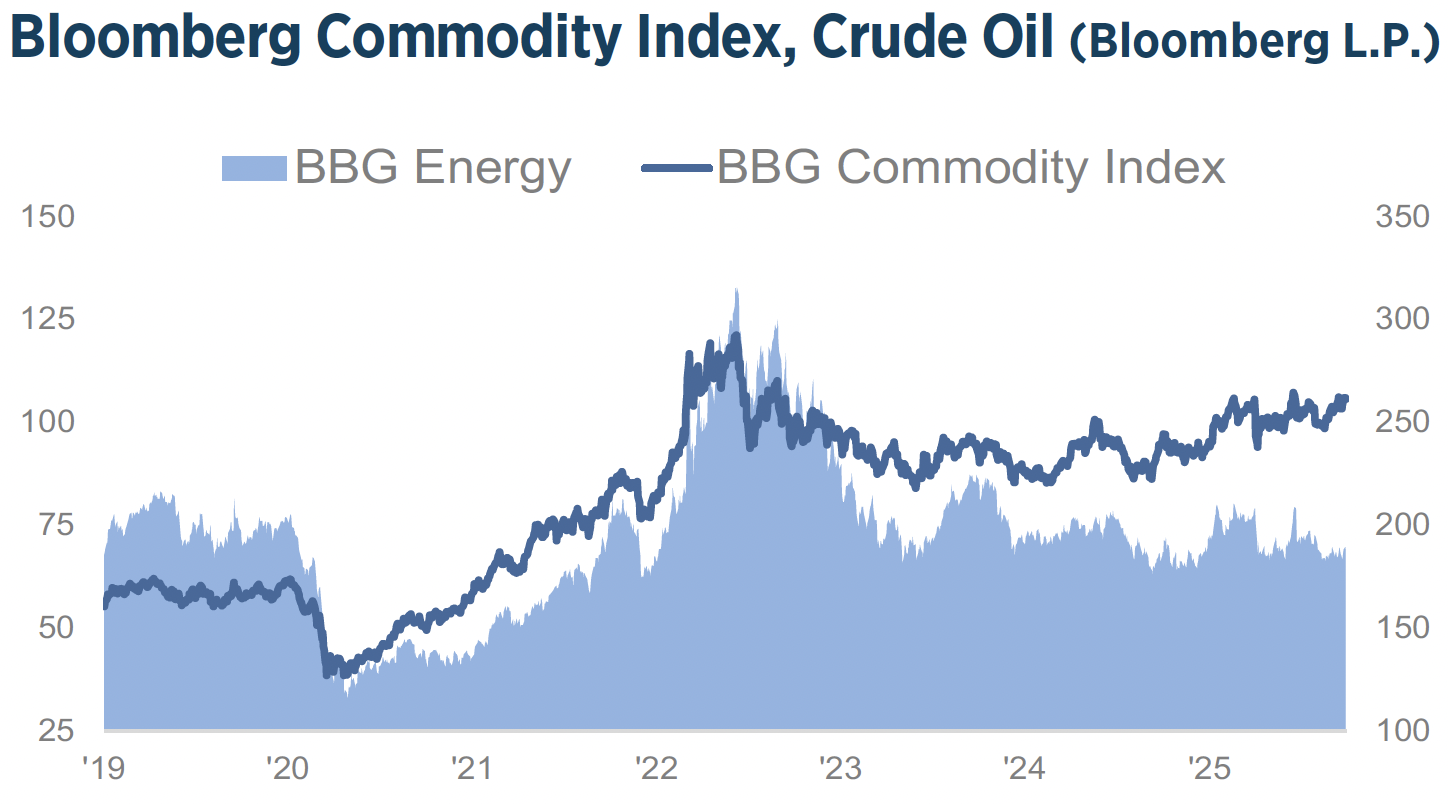

The Bloomberg Commodity Index was up 3.65% in Q3, +9.38% since the start of the year. The Precious Metals Index was up 19% and an astounding 48% since the start of the year.

Elevated levels of risk, such as fiscal deficits, trade tariffs and geopolitical concerns, continue to see investors favor the safe haven of precious metals. Gold reached its next milestone at $4’000 per ounce. The Bloomberg Energy Index was down 3.33% over the quarter, -4.45% since the start of the year. After higher-than-expected increase in oil output starting in August, OPEC+ decided for a modest November hike of 137k bpd.

The group’s restraint likely highlights growing unease about softening balances and limited demand support for 2026. We keep the recommended tactical allocation in commodities at neutral. We remain strategically positive on precious metals. Further, it’s still worth to bear in mind, that commodities as a group make up only somewhere between 1-3% of total global assets under management. Commodities remain a vastly under-owned cohort.

MACRO

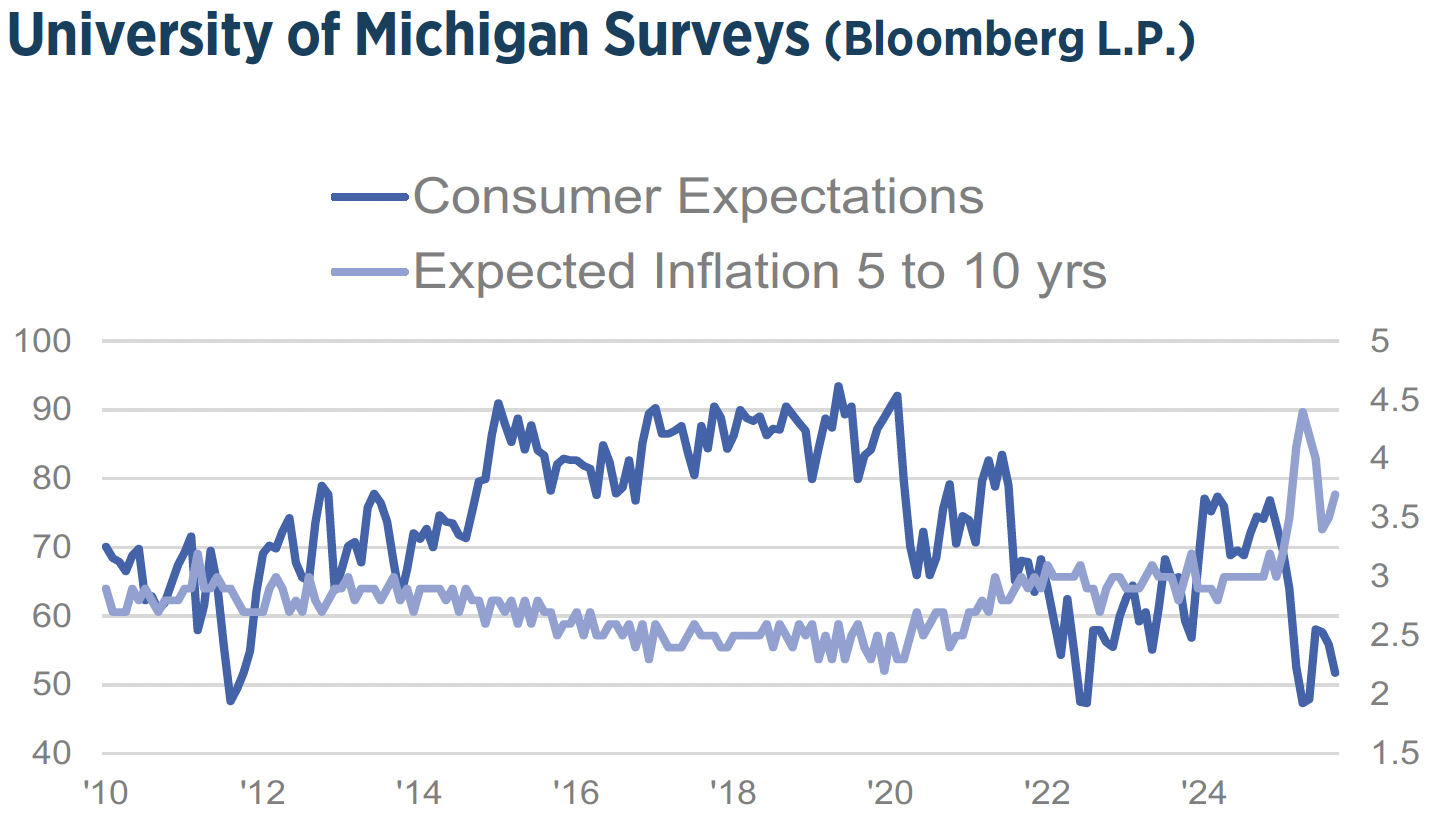

Market based inflation expectations, which are important to monitor, continue to stay closer to 2%. US headline inflation moved up to 2.9% y/y in August, after having fallen to as low as 2.3% in April. We were expecting tariffs to start to show up more visibly in the data, as the setup of tariffs, firm inventories, and CPI methodology all lead to a delayed pass-through into the official consumer price measure.

The FED’s preferred inflation gauge, PCE, was reported 2.9% y/y for August. This proves the stickiness of inflation above 2% target. We have pointed out before, that a post-peak globalization world will exhibit stagflationary tendencies. That growth will be lower than inflation. Investors face challenges in understanding the current US administration’s policies and philosophies. This is due to a lack of predictability and a unique approach that combines domestic and international issues. The key aspects to consider are, the administration takes a holistic view, connecting various matters into a single policy agenda.

It demonstrates flexibility in tactics while maintaining a focus on strategic goals. The administration is unbound by conventional wisdom, focusing on power sources and untapped opportunities. Trade policy exemplifies this. Traditional theory supports free trade for global efficiency and growth. The current administration’s approach considers improved trade terms, economic security, and addressing inequality. This suggests a broader policy perspective that goes beyond just tariffs and includes economics, foreign policy, politics, and culture.

It demonstrates flexibility in tactics while maintaining a focus on strategic goals. The administration is unbound by conventional wisdom, focusing on power sources and untapped opportunities. Trade policy exemplifies this. Traditional theory supports free trade for global efficiency and growth. The current administration’s approach considers improved trade terms, economic security, and addressing inequality. This suggests a broader policy perspective that goes beyond just tariffs and includes economics, foreign policy, politics, and culture.

A more comprehensive view is needed to evaluate the long-term impact on global economic activity and prices. A fundamental reorganization of the global economy along with its supply chains, energy systems and underlying technology foundations is taking place.

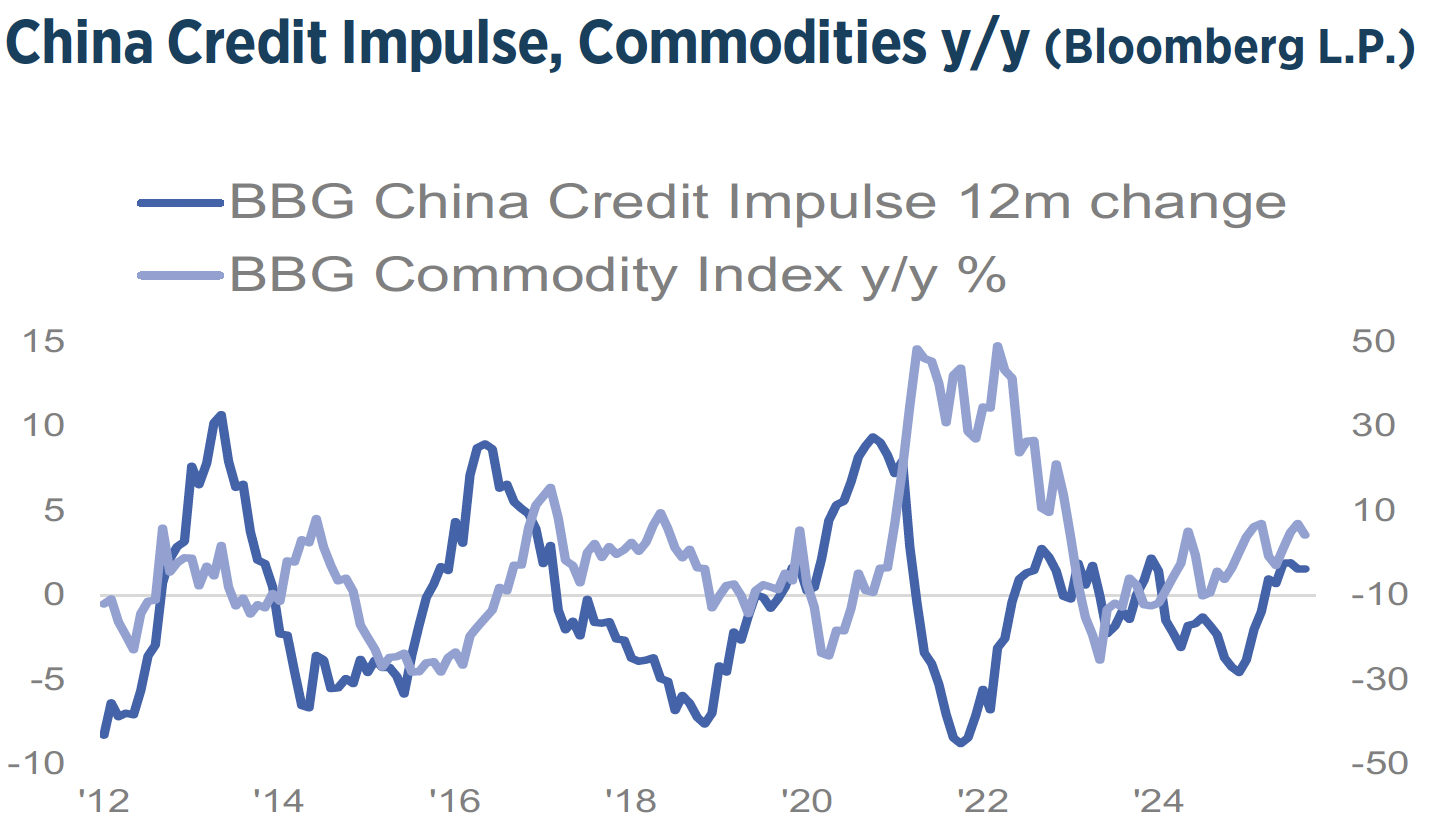

There is a strong connection between global liquidity and risky assets. Global liquidity is largely controlled by China on the one side and the FED, and increasingly the US Treasury, on the other. While the FED influences financial markets, the PBoC drives real economy and commodity cycles. Investors must therefore also closely watch China and its monetary policy actions.

Chinese liquidity is on the up. However, a resurging Dollar tempers global liquidity. We live in a debt-dominated world. Today financial markets serve as debt refinancing mechanism, more so than as a capital raising vehicles for new investments.

According to the World Bank 80% of credits are collateralbacked, at the heart of it are the repo markets, fundamental to the functioning of collateralized credit. The market structure has shifted, the interbank FED-funds market, which is unsecured, is now much smaller in importance than secured funding markets. It is no surprise, that in a recent paper the FED Dallas discussed considering the repo markets as a new operating target. Recent data show emerging imbalances between the supply of liquidity and the availability of good quality collateral.

TACTICAL ALLOCATION

The inflationary forces are structural and secular, on higher debt-load, demographics and on-shoring of manufacturing. We have been in an interim period for the past three years. Inflation risks have picked up at end of 2024. The market currently prices in 50 bps cuts for the remainder of 2025, and sees the ECB at the terminal rate. We recommend to increase the allocation in fixed income tactically to overweight, on US rate cuts prospect, driven by growth and labor market concerns. We prefer investment grade. We maintain high yield to neutral, however, we see a poor risk/reward in credit spreads and expect a slight widening. Selectivity and diversification are key. We are mindful of the developments in the commodities, for signs, should inflation risks accentuate.

The inflationary forces are structural and secular, on higher debt-load, demographics and on-shoring of manufacturing. We have been in an interim period for the past three years. Inflation risks have picked up at end of 2024. The market currently prices in 50 bps cuts for the remainder of 2025, and sees the ECB at the terminal rate. We recommend to increase the allocation in fixed income tactically to overweight, on US rate cuts prospect, driven by growth and labor market concerns. We prefer investment grade. We maintain high yield to neutral, however, we see a poor risk/reward in credit spreads and expect a slight widening. Selectivity and diversification are key. We are mindful of the developments in the commodities, for signs, should inflation risks accentuate.

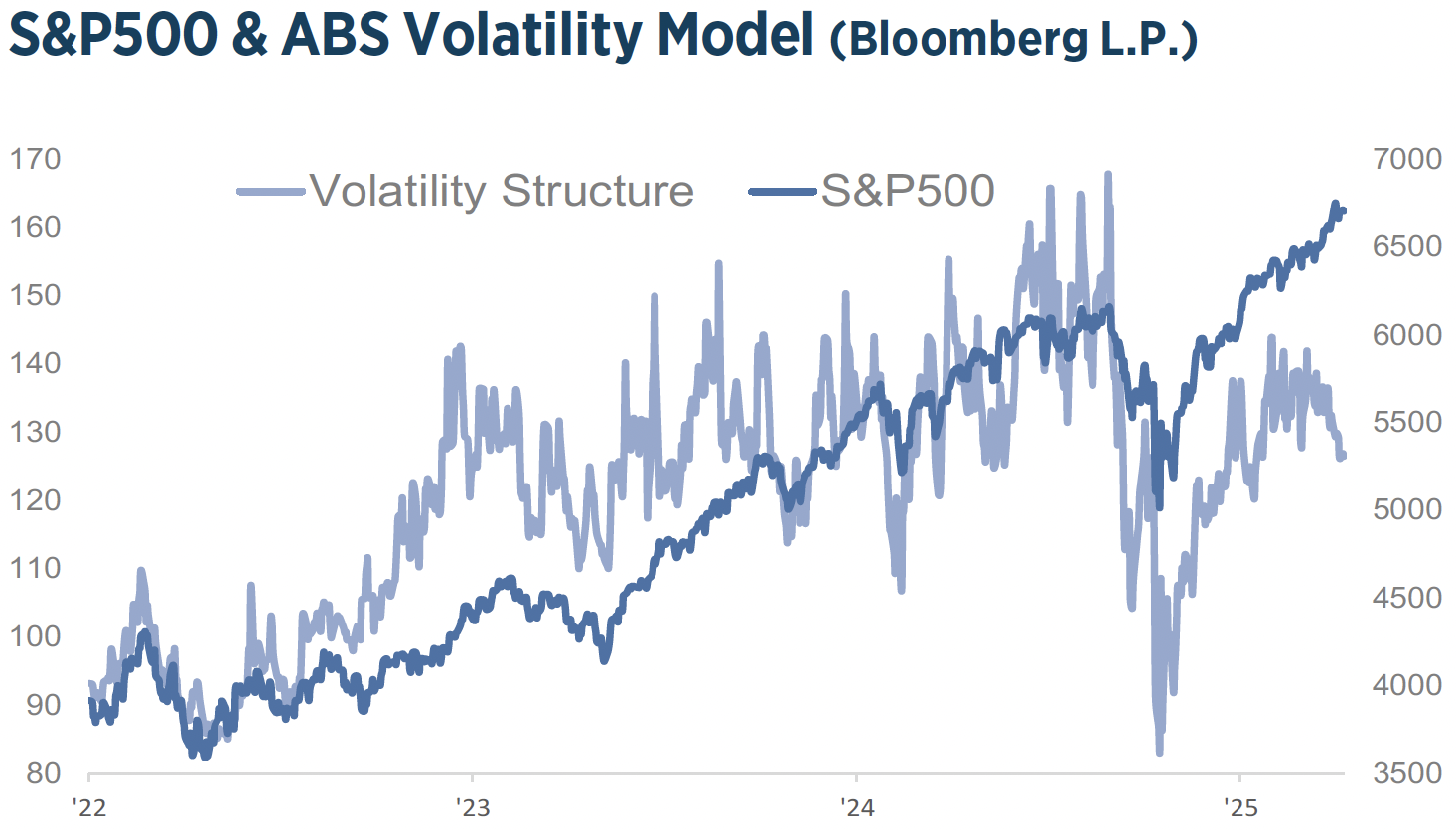

S&P500 & Volatility

The upswing in the investment cycle maybe 36 months old, if one counts from the low in October 2022, when the current liquidity cycle got started. But the investment climate is still mostly risk on. We believe equity markets are in a positive but delicate equilibrium, they can continue to go higher, but are increasingly sensitive to a broad range of macro and political factors. Asset allocation today is primarily driven by global liquidity. What is increasingly the result of government spending, respectively what can be termed fiscal dominance. Equity valuations are not cheap, with the forward 12-month P/E ratio for the S&P500 at 23, compared to the 5-year average of 20. However, rising AI capital expenditure will be supportive to valuations. Although current investor sentiment is neutral, US household allocation to stocks hit a record 45%. We maintain the allocation in equities to neutral, but remain vigilant. Things can change day-to-day. We are neutral on US and Europe and overweight to China. We focus on high quality and diversification remains key.

The upswing in the investment cycle maybe 36 months old, if one counts from the low in October 2022, when the current liquidity cycle got started. But the investment climate is still mostly risk on. We believe equity markets are in a positive but delicate equilibrium, they can continue to go higher, but are increasingly sensitive to a broad range of macro and political factors. Asset allocation today is primarily driven by global liquidity. What is increasingly the result of government spending, respectively what can be termed fiscal dominance. Equity valuations are not cheap, with the forward 12-month P/E ratio for the S&P500 at 23, compared to the 5-year average of 20. However, rising AI capital expenditure will be supportive to valuations. Although current investor sentiment is neutral, US household allocation to stocks hit a record 45%. We maintain the allocation in equities to neutral, but remain vigilant. Things can change day-to-day. We are neutral on US and Europe and overweight to China. We focus on high quality and diversification remains key.