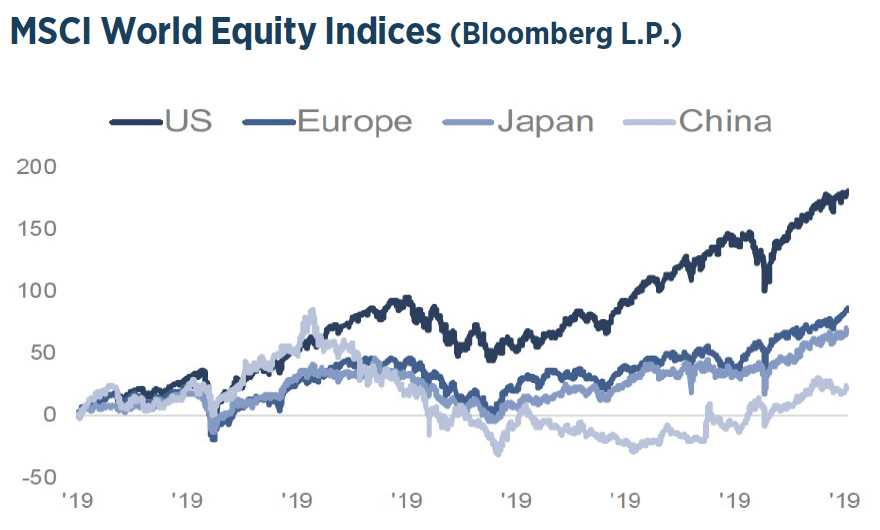

GLOBAL STOCK MARKETS

The year 2025 was marked by significant turbulence, characterized by high levels of political and geopolitical uncertainty. It underscored once again the dependence on the US, which accounts for roughly two-thirds of global market capitalization.

Despite these challenges, global equities delivered robust returns, driven by both large-cap leaders and smaller companies. AI-focused firms significantly contributed to this performance, while non-US sectors such as defense, Asian technology, and commodities outperformed the US market. The dominance of artificial intelligence has sparked discussions about a potential investment bubble, raising questions about how the capital expenditure boom is being financed.

Despite these challenges, global equities delivered robust returns, driven by both large-cap leaders and smaller companies. AI-focused firms significantly contributed to this performance, while non-US sectors such as defense, Asian technology, and commodities outperformed the US market. The dominance of artificial intelligence has sparked discussions about a potential investment bubble, raising questions about how the capital expenditure boom is being financed.

Temporary corrections are to be expected, as the S&P 500 recorded its third consecutive year of strong gains. This risk is inherent in every investment and can be managed through an appropriate long-term investment strategy, good

diversification, and adequate risk management.  The long-term opportunities outweigh the risks, and even after an excellent year, where risk-on sentiment drove an “everything-rally,” investors should not remain on the sidelines. The investment cycle in the AI sector is likely not yet over, and the US consumer remains robust. Exciting opportunities could also arise in China and Europe if government stimulus measures find their way into the real economy. Given the current investment environment, real assets are likely to remain among the most sought-after asset classes in 2026.

The long-term opportunities outweigh the risks, and even after an excellent year, where risk-on sentiment drove an “everything-rally,” investors should not remain on the sidelines. The investment cycle in the AI sector is likely not yet over, and the US consumer remains robust. Exciting opportunities could also arise in China and Europe if government stimulus measures find their way into the real economy. Given the current investment environment, real assets are likely to remain among the most sought-after asset classes in 2026.

Our strategies for the start of the year continue to focus on equities. Bonds are less attractive given the interest rate environment but should still offer tactical opportunities. Precious metals remain an important addition to a portfolio. Markets are shifting focus from exciting narratives to tangible financial performance results. It requires the balance of longterm growth themes with protection against volatility.

Fundamentals and discipline will become important again. The last year brought a meaningful change. The world faces a prolonged shift toward protectionism and regionalization, along with increased defense and infrastructure spending. This shift may uncover value in sectors beyond traditional tech giants. Looking into 2026, we see several supportive elements for an acceleration of global economic growth.

Fundamentals and discipline will become important again. The last year brought a meaningful change. The world faces a prolonged shift toward protectionism and regionalization, along with increased defense and infrastructure spending. This shift may uncover value in sectors beyond traditional tech giants. Looking into 2026, we see several supportive elements for an acceleration of global economic growth.

The US will start to benefit from the OBBBA tax cuts and capital investments. We can expect the current US administration to seek ways to support consumers ahead of the November midterm elections. Similarly, the European and Japanese economies will be supported, while China’s new 15th Five-Year Plan (2026-2030) will be in focus too. In conclusion, the investment landscape in 2026 presents both challenges and opportunities.

The US will start to benefit from the OBBBA tax cuts and capital investments. We can expect the current US administration to seek ways to support consumers ahead of the November midterm elections. Similarly, the European and Japanese economies will be supported, while China’s new 15th Five-Year Plan (2026-2030) will be in focus too. In conclusion, the investment landscape in 2026 presents both challenges and opportunities.

GLOBAL FIXED INCOME MARKETS

Major central banks shifted into easing monetary policy. The FED initiated rate cuts in September, ending the year with three reductions as labor markets softened. Bringing the target range to 3.75% and 3.50%. By June, the ECB lowered the deposit rate from 3% to 2%. On the opposite side, the Bank of Japan had to increase its target rate from 0.25% to 0.75%, as inflation is uncomfortably high.

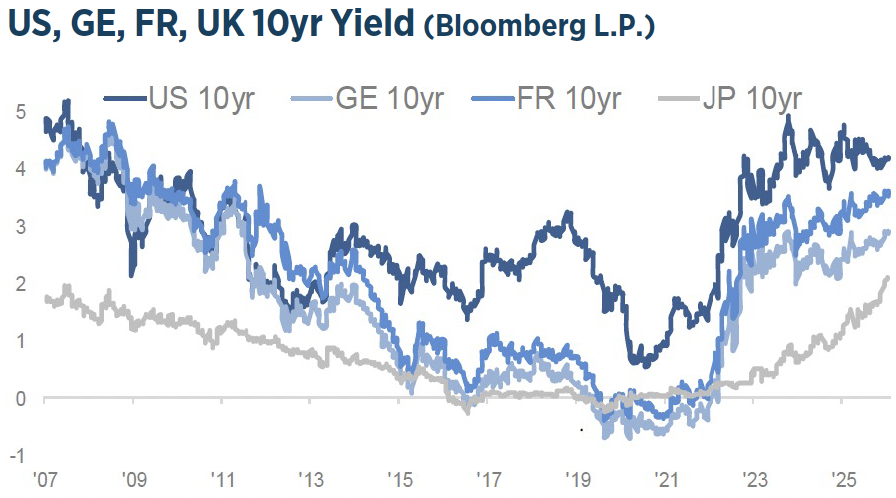

The US 10- year Treasury yield ended 2025 at 4.16%, down from 4.56% at the start of the year. A “risk-on” sentiment prevailed across asset classes, resulting in an “everything rally” where all major asset classes delivered positive returns for the first time since the pandemic. The Bloomberg US Aggregate Bond Index rose by 7.3% return. US fixed income outperformed most developed markets. The German 10-year Bund yield rose from 2.36% to 2.85%. The Japanese 10-year JGB from 1.10%to 2.06%.

The US 10- year Treasury yield ended 2025 at 4.16%, down from 4.56% at the start of the year. A “risk-on” sentiment prevailed across asset classes, resulting in an “everything rally” where all major asset classes delivered positive returns for the first time since the pandemic. The Bloomberg US Aggregate Bond Index rose by 7.3% return. US fixed income outperformed most developed markets. The German 10-year Bund yield rose from 2.36% to 2.85%. The Japanese 10-year JGB from 1.10%to 2.06%.

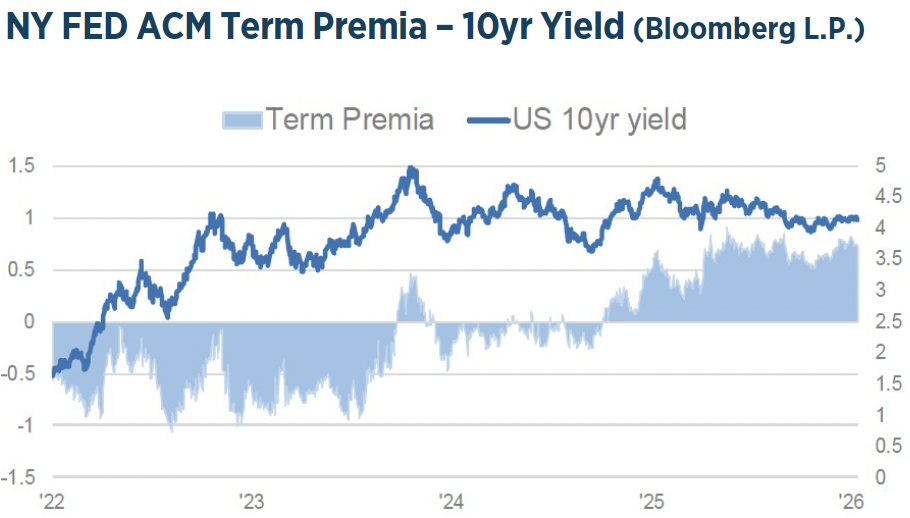

Fiscal concerns continued to weigh on government bonds, particularly in Europe and Japan. Global credit markets have been running hot. Yield premiums on corporate debt have narrowed to the lowest since 2007. Investment grade and high yield corporate bonds saw strong demand due to good corporate fundamentals and attractive all-in yields.

Mortgage-backed securities outperformed corporate bonds. The feared tariff-driven inflation spike failed to materialise, instead the weakening of the labour market paved the way for the FED to lower rates. For 2026 we only see the need for one 25bps cut as the economy accelerates on fiscal stimulus. One source of uncertainty for investors come from the wide range of forecasts in the FED’s dot plot, reflecting unusually divisive members, with opposing economic and political views.

The spread between the low and high estimate for 2026 has widened to 175bps. Incoming economic data will be scrutinized. The announcement of the new FED Chairman, and his intentions, will be critical too. The FED is challenged by the decoupling of US GDP growth from evidently sluggish jobs creation. The third quarter GDP accelerated to an annualized 4.3% pace, while Nonfarm payrolls have flatlined. The FED needs to adapt to the economic transformation. Its data-dependent approach is no longer up-to-date.

The spread between the low and high estimate for 2026 has widened to 175bps. Incoming economic data will be scrutinized. The announcement of the new FED Chairman, and his intentions, will be critical too. The FED is challenged by the decoupling of US GDP growth from evidently sluggish jobs creation. The third quarter GDP accelerated to an annualized 4.3% pace, while Nonfarm payrolls have flatlined. The FED needs to adapt to the economic transformation. Its data-dependent approach is no longer up-to-date.

US DOLLAR

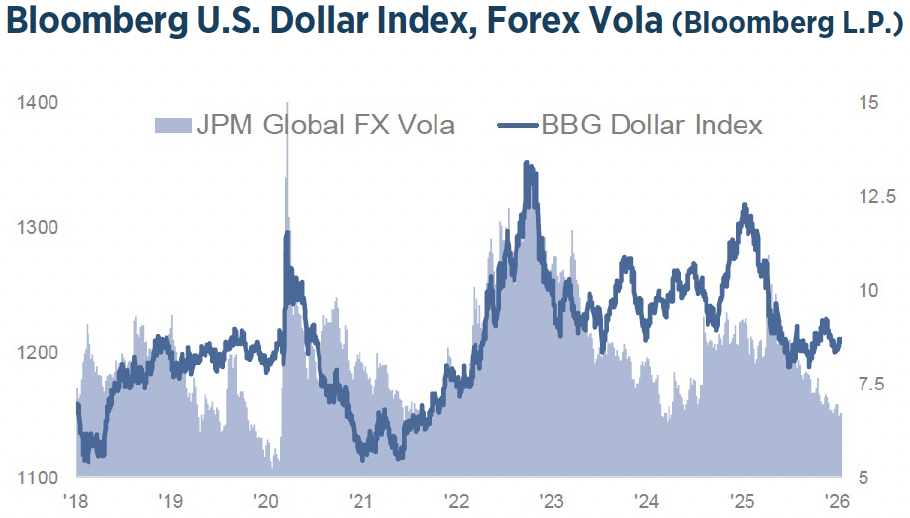

After the Dollar had fallen 10% from its peak last February, it drifted higher for the second half of the year. Calls for de-dollarization in the face of escalating tariff wars were increasing. Many saw the end of the US Dollar as a reserve currency and safe haven. Yet, capital inflows into US asset remained. Despite the many unknowns hanging over the financial markets, geopolitics, FED independence, political risks and the present threats of an intervention, volatility in FX markets has stayed very low. Although the Dollar’s share of global foreign exchange reserves has declined from over 65% to 58% over the past 10 years, there is no getting around the US capital market and the dominant role of the Dollar in the global reserve system in the foreseeable future.

Although the Dollar’s share of global foreign exchange reserves has declined from over 65% to 58% over the past 10 years, there is no getting around the US capital market and the dominant role of the Dollar in the global reserve system in the foreseeable future.

However, it’s clear that a shift towards a more multipolar global monetary system is underway, with the US and China utilizing different strategies to gain influence. The US is embracing financial technology. The US regulatory approach is leaning on the development of Dollar-pegged stablecoins. China is working to internationalize the Yuan and gradually reduce reliance on the Dollar by using a dual strategy of accumulating Gold and promoting its own digital currency, e-CNY. The year 2026 is shaping up to be a very interesting one for the FXmarkets.

COMMODITIES

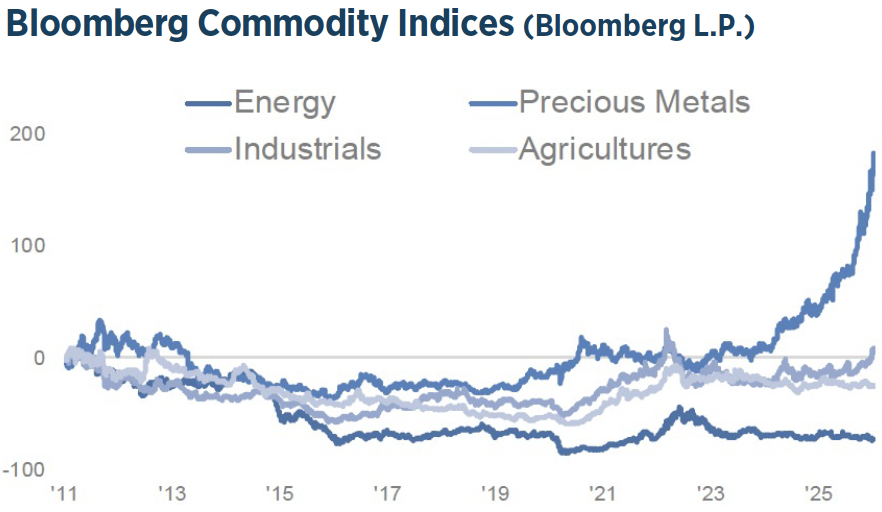

The Bloomberg Commodity Index was up 11% in 2025.

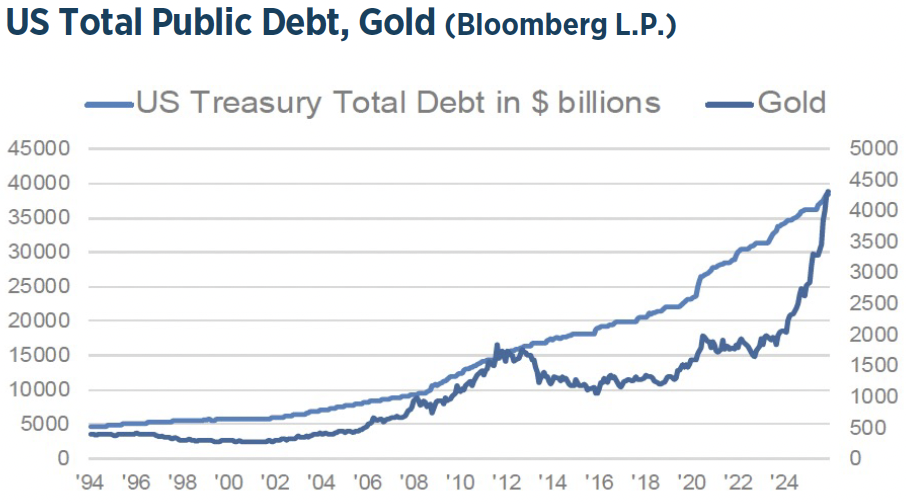

The Precious Metals Index increased by 73%, with Silver rising an astounding 147%. Elevated levels of risk, such as fiscal deficits, trade tariffs and geopolitical concerns, continue to see investors favor the safe haven of precious metals.

Silver’s surge was intensified when the US designated it as a critical mineral and China imposed stricter export controls, heightening fears of supply chain disruptions and prompting physical stockpiling. The Bloomberg Energy Index fell 14% in 2025. OPEC+ has shifted toward a cautious «wait-and-see» strategy, deciding to pause all planned production increases through March. In 2025, OPEC+ increased its total oil output targets by approximately 2.9 million bpd.

The US intervention in Venezuela has only a limited bearish impact on oil, however, the geopolitical signal is significant. The market structure has since moved to a steeper backwardation, implying tightness of supply. At the same time, a large speculative positioning in WTI Crude futures indicates a bearish positioning, that could be vulnerable to reversal, increasing upside asymmetry. We keep the recommended tactical allocation in commodities at neutral. We remain strategically positive on precious metals. Further, it’s still worth to bear in mind, that commodities as a group remain a vastly under-owned cohort.

The US intervention in Venezuela has only a limited bearish impact on oil, however, the geopolitical signal is significant. The market structure has since moved to a steeper backwardation, implying tightness of supply. At the same time, a large speculative positioning in WTI Crude futures indicates a bearish positioning, that could be vulnerable to reversal, increasing upside asymmetry. We keep the recommended tactical allocation in commodities at neutral. We remain strategically positive on precious metals. Further, it’s still worth to bear in mind, that commodities as a group remain a vastly under-owned cohort.

MACRO

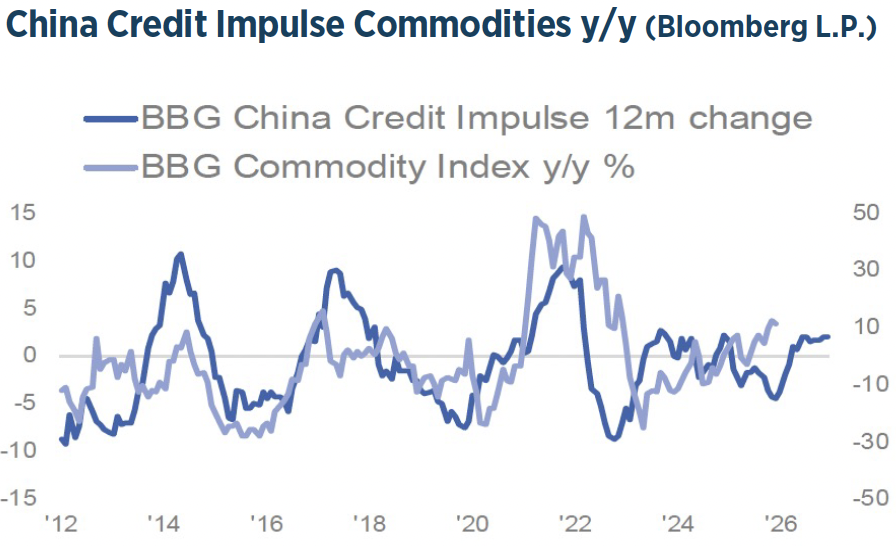

US headline inflation was reported at 2.7% for December, down from 3% in September. The FED’s preferred inflation gauge, PCE, has not been reported since the September data, due to the US government shutdown. The US disinflation trend has not reversed, however, the progress has stalled. This proves the stickiness of inflation above 2% target. We have pointed out before, that a post-peak globalization world will exhibit stagflationary tendencies. That growth will be lower than inflation. Looking ahead, measures of global liquidity show, that the US funding cycle has peaked, what has led the FED to end its quantitative tightening.  At the December meeting the FED announced its Reserve Management Purchases program of monthly purchases of short-term Treasuries of around $40 billion, to maintain an ample level of reserves in the banking systems. On the other hand, measures show, that China embarked on a new liquidity cycle. While the US liquidity cycle is more beneficial to the financial markets, China has more impact on the real economies, due to its large industrial footprint. As the global economy is to improve, business activity will redirect liquidity away from financial markets.

At the December meeting the FED announced its Reserve Management Purchases program of monthly purchases of short-term Treasuries of around $40 billion, to maintain an ample level of reserves in the banking systems. On the other hand, measures show, that China embarked on a new liquidity cycle. While the US liquidity cycle is more beneficial to the financial markets, China has more impact on the real economies, due to its large industrial footprint. As the global economy is to improve, business activity will redirect liquidity away from financial markets.

Looking at 2026 requires to understand, that the geopolitical change impacts trade, security and energy. A new technological race has started. So-called geopolitical camp formations are reshaping how the world works. As a consequence, a redesign of supply chains asks for significant capital expenditures in energy, grid infrastructure, AI and defense, what will create winners and loosers. Today investors are surounded by an enormous amount of uncertainty. The financial markets had, and have to weather and tolerate all kinds of unconventional policies in the past year.

Looking at 2026 requires to understand, that the geopolitical change impacts trade, security and energy. A new technological race has started. So-called geopolitical camp formations are reshaping how the world works. As a consequence, a redesign of supply chains asks for significant capital expenditures in energy, grid infrastructure, AI and defense, what will create winners and loosers. Today investors are surounded by an enormous amount of uncertainty. The financial markets had, and have to weather and tolerate all kinds of unconventional policies in the past year. Policy is increasingly determining market behaviour, with decisions on spending, taxes and trade having an impact on various areas of the financial markets.

Policy is increasingly determining market behaviour, with decisions on spending, taxes and trade having an impact on various areas of the financial markets.

Policy risk has become central to investment management. The interconnected challenges of rate transitions, fiscal pressures, and regulation are shaping portfolios in real time. A fundamental reorganization of the global economy along with its supply chains, energy systems and underlying technology foundations is taking place.

TACTICAL ALLOCATION

The inflationary forces are structural and secular, on higher debt-load, demographics and on-shoring of manufacturing. We have been in an interim period for the past three years, however: the disinflation progress has stalled. Inflation risks have not gone away. The market currently prices in 50 bps cuts for 2026 in the US, and sees the ECB at the terminal rate.

The inflationary forces are structural and secular, on higher debt-load, demographics and on-shoring of manufacturing. We have been in an interim period for the past three years, however: the disinflation progress has stalled. Inflation risks have not gone away. The market currently prices in 50 bps cuts for 2026 in the US, and sees the ECB at the terminal rate.

We recommend to cut the allocation in fixed income tactically to underweight. We only see the need for one 25 bps cut, as fiscal stimulus will be supportive, and more measures can be expected ahead of the US mid-term elections. Fiscal worries around Europe and Japan will persist, what will continue to drive term premia higher. Less so in the US. We prefer investment grade. We maintain high yield to neutral, however, we see a poor risk/reward in credit spreads. Private credit concerns remain, but the near-term outlook seem not to deteriorate sharply. Overall, selectivity and diversification are key. We are mindful of the developments in the commodities, particularly in energy for signs, should inflation risks accentuate.

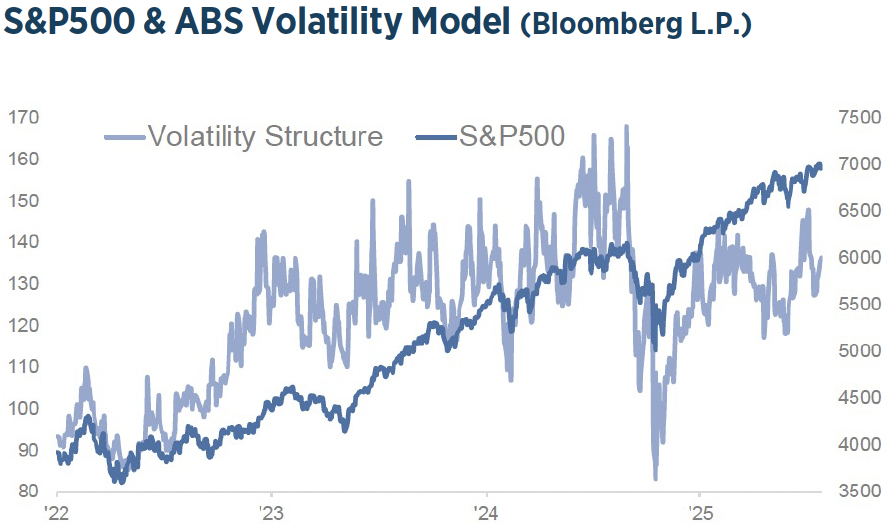

S&P500 & VOLATILITY

The upswing in the investment cycle is now 39 months old, if one counts from the low in October 2022, when the current liquidity cycle started. Based on market activity in early 2026, a significant “Great Rotation” is underway, moving capital out of US megacap tech stocks into smaller-cap, value-oriented and international equities. The rotation should be also reinforced by economic drivers. Asia sees burgeoning confidence across the region. The focus turns to global “shovel” assets, energy, grid, automation and AI compute. Markets are still in a positive but delicate equilibrium, they can continue to go higher, but have become more sensitive to a broad range of macro and political factors. Equity valuations are not cheap, with the forward 12-month P/E ratio for the S&P500 at 23, compared to the 5-year average of 20. We maintain the allocation in equities to neutral, but remain vigilant. We are neutral on US and Europe and overweight to China. By focusing on fundamentals and maintaining discipline, investors can navigate the complexities of the market and capitalize on the opportunities that arise.

The upswing in the investment cycle is now 39 months old, if one counts from the low in October 2022, when the current liquidity cycle started. Based on market activity in early 2026, a significant “Great Rotation” is underway, moving capital out of US megacap tech stocks into smaller-cap, value-oriented and international equities. The rotation should be also reinforced by economic drivers. Asia sees burgeoning confidence across the region. The focus turns to global “shovel” assets, energy, grid, automation and AI compute. Markets are still in a positive but delicate equilibrium, they can continue to go higher, but have become more sensitive to a broad range of macro and political factors. Equity valuations are not cheap, with the forward 12-month P/E ratio for the S&P500 at 23, compared to the 5-year average of 20. We maintain the allocation in equities to neutral, but remain vigilant. We are neutral on US and Europe and overweight to China. By focusing on fundamentals and maintaining discipline, investors can navigate the complexities of the market and capitalize on the opportunities that arise.